Filatex Fashions Limited is a small textile company known mainly for socks manufacturing. It attracts attention because it operates in a niche business, has a very low share price, and often stays on the radar of traders looking for turnaround stories. At the same time, the stock is highly risky, and its financial performance has become weaker in the latest period. The textile and apparel sector in India still has long-term demand potential, but company-level execution matters much more than sector headlines. In this article, we will look at Filatex Fashions’ business, latest financial position, shareholding, price history, growth factors, risks, and realistic share price target estimates from 2026 to 2050 in simple language.

Filatex Fashions Limited Company Overview

| Company Essential | Value |

|---|---|

| Market Cap | ₹158.35 Cr. |

| Enterprise Value | ₹217 Cr. (Approx.) |

| No. of Shares | 833.41 Cr. |

| P/E | 53.70 |

| P/B | 0.07 |

| Face Value | ₹1 |

| Book Value | ₹2.78 |

| Debt | ₹0.45 Cr. (Approx.) |

| Sales Growth | -64.25% (Latest YoY Quarter) |

| ROE | 0.41% |

| Dividend Yield | 0.00% |

What Does Filatex Fashions Limited Do?

Filatex Fashions Limited mainly works in the socks and hosiery segment. The company manufactures socks and related textile products for domestic and export markets. Its business model is based on producing quality socks in different materials such as cotton, woolen, and other blended fabric categories. It also has its own brands, including Smartman and Tuscany, which help it build identity in the Indian market. Revenue comes from manufacturing, branded sales, and customer supply relationships. The company operates in a niche part of the textile industry, which can be an advantage because socks are a repeat-purchase product. Its long-term strategy seems to depend on improving scale, using modern production technology, growing its market presence, and building stronger profitability over time.

Historic Share Price Performance

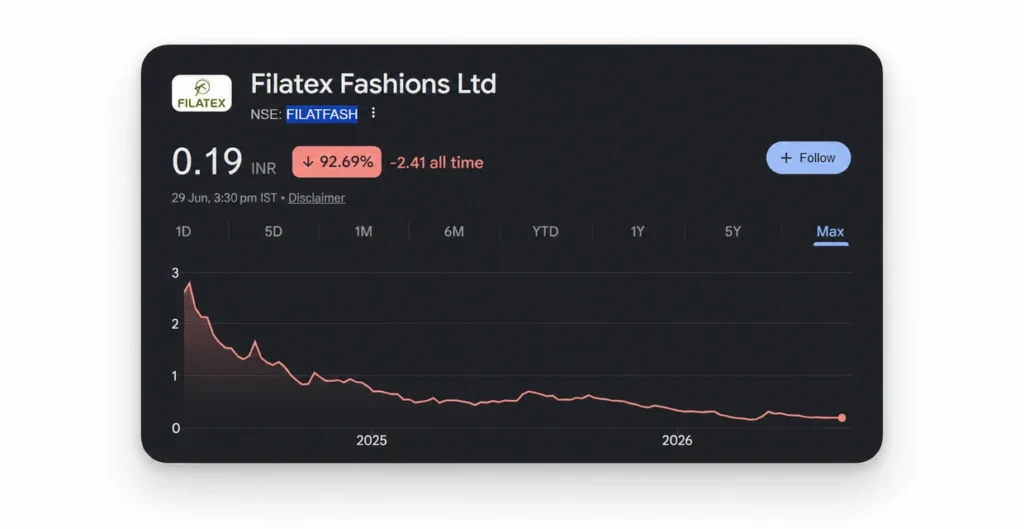

Filatex Fashions has had a highly volatile stock market journey. It is not a stable compounder-type stock. Instead, it has moved through sharp rallies, deep corrections, and long weak phases. The share split in 2024 changed the face value from ₹5 to ₹1, which also changed how the stock appeared to retail investors. During 2025, the stock remained very active but corrected heavily by year-end. In 2026, the stock stayed under pressure and traded near penny-stock levels around ₹0.19–₹0.20. Recent weakness in earnings and major changes in shareholding structure also affected sentiment. Overall, the historical trend shows that the stock can move sharply in the short term, but long-term wealth creation has not yet become stable. Investors should treat past spikes as speculative moves, not proof of strong business quality.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2025 | ₹0.73 | ₹0.27 | -63.01% |

| 2026 (YTD) | ₹0.32 | ₹0.19 | -40.63% |

Latest Shareholding Pattern

Filatex Fashions Limited Shareholding Pattern

| Shareholder | Holding |

|---|---|

| Promoters | 5.11% |

| FIIs | 0.79% |

| DIIs | 0.00% |

| Public | 94.11% |

| Others | 0.00% |

Growth Factors

- The Indian textile and apparel market is large, and socks remain a regular demand product in both domestic and export channels.

- A niche position in socks manufacturing can help the company focus better than a broad textile player.

- Any recovery in export demand can support revenue growth if order flow improves.

- Better use of manufacturing capacity can improve margins because fixed costs get spread over larger sales.

- The company already has established brands, which can help if distribution expands in India.

- Use of modern production technology can support quality and reduce wastage over time.

- If management improves working capital control, the business can become more efficient and less fragile.

- Any successful use of proposed fundraising can support expansion, procurement, or operational strengthening.

- The low base of current earnings means even moderate improvement can create visible percentage growth.

- If the company builds a stronger balance between exports, brands, and contract supply, long-term business stability may improve.

Filatex Fashions Limited Share Price Target 2026 To 2050

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹0.14 | ₹0.24 | ₹0.33 |

| 2027 | ₹0.18 | ₹0.23 | ₹0.27 |

| 2028 | ₹0.25 | ₹0.15 | ₹0.10 |

| 2029 | ₹0.11 | ₹0.14 | ₹0.17 |

| 2030 | ₹0.19 | ₹0.24 | ₹0.40 |

| 2035 | ₹0.42 | ₹0.54 | ₹0.66 |

| 2040 | ₹0.70 | ₹0.63 | ₹0.58 |

| 2050 | ₹0.98 | ₹0.75 | ₹0.69 |

Also Check:

- Tilak Ventures Ltd Share Price Target

- LCC Infotech Share Price Target

- M K Proteins Ltd Share Price Target

- Shalimar Productions Ltd Share Price Target

- K Lifestyle Share Price Target

Filatex Fashions Limited Share Price Target 2026

The 2026 estimate is kept cautious because the company is coming after a weak earnings phase and the stock is still trading at a very low level. If business stabilizes, revenue decline slows, and market sentiment improves, the stock may attempt a recovery from current levels. But if earnings remain weak, upside may stay limited. This target range assumes no major negative surprise in operations and no extreme dilution pressure in the near term.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹0.14 |

| Second Half | ₹0.33 |

Filatex Fashions Limited Share Price Target 2030

By 2030, the stock can do better only if the business shows consistent sales growth, margin recovery, and a clearer balance sheet story. A small company can re-rate quickly when profits improve, but that also depends on governance confidence and capital allocation. The 2030 range assumes the company survives this weak phase, expands gradually, and avoids excessive destruction of shareholder value. It is a possibility-based estimate, not a promise.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹0.19 |

| Second Half | ₹0.40 |

Filatex Fashions Limited Share Price Target 2035

The 2035 projection assumes that Filatex Fashions becomes a steadier niche textile player with better profits than today. For that to happen, management will need stronger execution, better return ratios, and more predictable sales. Brand strength, export revival, and cleaner financial quality can support valuation improvement. However, because the company is very small today, long-term forecasting has high uncertainty. This target should be read as a scenario, not as a fixed expected outcome.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹0.42 |

| Second Half | ₹0.66 |

Filatex Fashions Limited Share Price Target 2040

A 2040 target is meaningful only if the company remains operationally relevant for many years and compounds business value slowly. In the best case, a niche socks player with disciplined operations and healthy margins can earn a better valuation than today. But there are also many things that can go wrong over such a long period. The 2040 estimate assumes survival, moderate growth, and no major long-term governance breakdown or repeated heavy dilution.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹0.70 |

| Second Half | ₹0.58 |

Filatex Fashions Limited Share Price Target 2050

The 2050 estimate is the most uncertain part of this article. Over such a long period, industry changes, management decisions, competition, regulation, and capital structure changes can completely reshape the company. The upside exists only if Filatex Fashions improves from a weak small-cap textile stock into a durable and profitable niche manufacturer. Even then, returns may not be smooth. This long-term range should be treated only as a broad hypothetical framework.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹0.98 |

| Second Half | ₹0.69 |

Bull Case

- The company operates in a focused niche rather than a very broad textile segment.

- Socks are a repeat-demand product with both domestic and export potential.

- A low earnings base means even a small operational improvement can lift profits sharply in percentage terms.

- The stock trades far below book value, which may attract deep-value speculation.

- Any successful use of new capital can improve scale or working capital strength.

- Established brands like Smartman and Tuscany give the company some market identity.

- Recovery in textile demand can support better utilization and stronger margins.

- If confidence in management and financial quality improves, valuation can re-rate from depressed levels.

Bear Case

- The stock is a penny-stock category name and carries very high volatility.

- Latest annual financial performance looks much weaker than the previous year.

- Return ratios such as ROE remain extremely low.

- Promoter holding has fallen sharply, which can worry long-term investors.

- Public holding is very high, which can increase speculative trading behavior.

- Any fundraising through convertible instruments can lead to dilution risk.

- The company is small and may struggle against larger textile players with stronger balance sheets.

- Long-term projections are highly uncertain because the current business quality is not yet strong enough.

Pros and Cons

Pros

- Focused business in socks and hosiery

- Presence in both domestic and export-oriented markets

- Brand names already exist in the portfolio

- Very low debt compared with many weak small companies

- Any turnaround can create fast percentage growth from a low base

Cons

- Very weak recent stock performance

- Latest earnings trend is soft

- Extremely low ROE and modest operating strength

- Sharp reduction in promoter holding raises concern

- High-risk, speculative nature makes long-term confidence difficult

Expert Opinion

Filatex Fashions Limited is a very high-risk small-cap textile stock, and its current valuation cannot be judged only by low price per share. The bigger issue is business quality, earnings consistency, and capital allocation. Long-term potential exists only if revenue stabilizes, margins improve, and management builds stronger confidence after recent changes in shareholding and fundraising plans. This stock may suit only investors who understand speculative small-cap risk and can tolerate deep volatility. Important things to monitor are sales trend, net profit trend, cash flow, book value movement, dilution risk, and whether return ratios improve meaningfully over the next few years.

Conclusion

Filatex Fashions Limited has a real operating business in a niche textile segment, and that gives it some long-term possibility. The company has product focus, manufacturing experience, and some brand presence. However, the latest numbers show that the business is currently not in a strong phase, and the stock remains highly speculative. That is why the share price targets in this article are kept conservative. The long-term opportunity depends on execution, profit recovery, balance sheet discipline, and investor trust. In short, Filatex Fashions can improve from current levels, but it remains a risky stock that should be tracked with caution.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

Is Filatex Fashions Limited a good long-term investment?

It is not a simple long-term stock for most investors because the business is small, returns are low, and price volatility is very high. It may interest high-risk investors looking for a possible turnaround story, but it is not yet a proven quality compounder.

What are the major risks of investing in Filatex Fashions Limited?

The main risks are weak earnings, low return ratios, high stock volatility, possible dilution, and uncertainty created by sharp changes in promoter holding. Another important risk is that the company may take longer than expected to improve business performance.