Indian Railway Catering and Tourism Corporation Limited, popularly known as IRCTC, is one of India’s most recognised railway-related public sector companies. It operates in online train ticketing, railway catering, Rail Neer packaged drinking water, tourism packages, hotels, and other travel-related services.

Investors follow IRCTC because of its strong brand, large railway passenger base, digital ticketing business, high profit margins, and government ownership. The company benefits when rail travel, tourism, premium trains, and online booking activity increase.

This article explains IRCTC’s business, financial performance, shareholding pattern, historic stock movement, growth opportunities, risks, and estimated IRCTC share price targets from 2026 to 2050.

Company Overview & Financial Highlights

| Company Essential | Value |

|---|---|

| Market Cap | ₹40,800 Cr. (Approx.) |

| Enterprise Value | ₹40,900 Cr. (Approx.) |

| No. of Shares | 80.00 Cr. |

| P/E | 29.3 |

| P/B | 9.5 |

| Face Value | ₹2 |

| Book Value | ₹53.86 |

| Debt | ₹90 Cr. (Approx. – Very Low Debt) |

| Sales Growth | 15% (TTM) |

| ROE | 32.34% |

| Dividend Yield | 1.74% |

IRCTC reported revenue growth of around 11.5% in FY2026, while net profit increased by nearly 6% compared with FY2025. The company remains almost debt-free and continues to generate strong cash flow from its internet ticketing business.

What Does IRCTC Do?

IRCTC is the main digital railway-ticketing platform connected with Indian Railways. It earns revenue from convenience fees, transaction-related services, travel bookings, catering contracts, Rail Neer bottled water, tourism packages, hotels, flights, buses, lounges, and other passenger services.

Its biggest strength is the online ticketing segment. This business requires relatively low capital compared with physical catering operations and generally gives better profitability. IRCTC also manages onboard catering, railway food plazas, e-catering, premium train meals, tourism trains, holiday packages, and religious tour packages.

The company has a strong position because of its deep connection with the Indian railway ecosystem. Its future strategy is likely to focus on digital services, premium travel, tourism growth, customer convenience, payment solutions, and expanding passenger-related services.

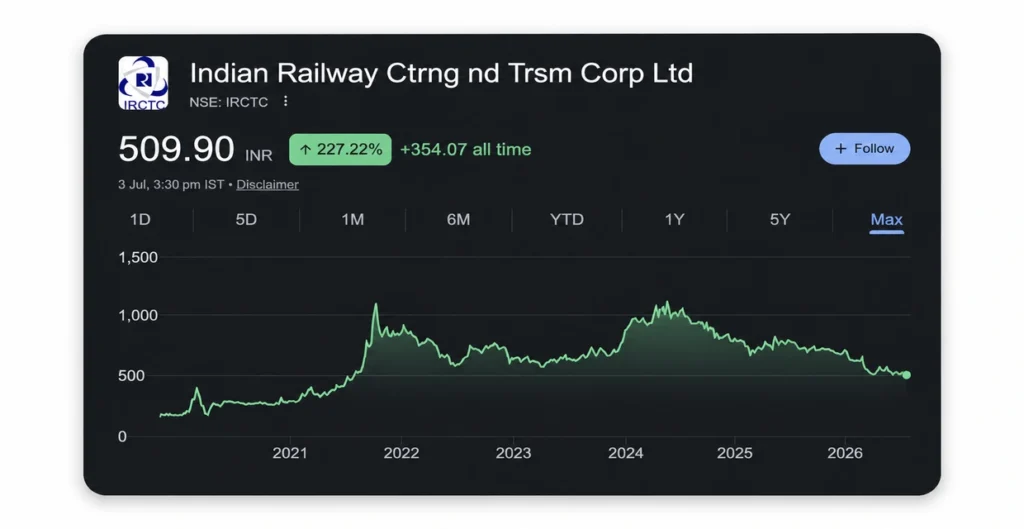

Historic Share Price Performance

IRCTC has experienced both strong rallies and sharp corrections since listing. The stock saw a major re-rating during the post-pandemic travel recovery phase as investors expected growth in railway travel, ticketing, tourism, and government-led railway development.

The share also faced corrections when profit growth slowed, valuations became expensive, or market sentiment towards railway stocks weakened. In 2023, IRCTC recovered strongly, but the stock again faced pressure in 2024, 2025, and early 2026.

The company’s business has remained profitable, but the market has become more careful about valuation. Long-term investors should understand that even strong companies can face deep corrections when earnings growth does not match high market expectations.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2021 | ₹278 | ₹796 | 186.0% |

| 2022 | ₹830 | ₹615 | -26.0% |

| 2023 | ₹612 | ₹863 | 41.1% |

| 2024 | ₹951 | ₹773 | -18.7% |

| 2025 | ₹807 | ₹681 | -15.7% |

| 2026 YTD | ₹620 | ₹510 | -17.7% |

The table uses rounded adjusted monthly reference prices. IRCTC’s FY2026 performance remained positive despite share-price weakness during the year.

Latest Shareholding Pattern

| Shareholder | Holding |

|---|---|

| Promoters | 62.40% |

| FIIs | 4.86% |

| DIIs | 14.86% |

| Public | 17.88% |

| Others | 0.00% |

The Government of India remains the main shareholder through the President of India. Domestic institutional ownership has increased over time, while foreign institutional ownership has reduced in the latest reported quarter.

Growth Factors

- Strong railway ecosystem position: IRCTC remains closely linked with India’s railway passenger system. Growth in train travel can support ticketing, catering, tourism, and food services.

- Internet ticketing strength: Online ticketing is one of IRCTC’s most profitable segments. Higher digital adoption, mobile booking, UPI usage, and smartphone penetration can support long-term growth.

- Premium train opportunities: Vande Bharat, Tejas, premium trains, and tourist trains can improve catering demand and passenger spending.

- Tourism expansion: Religious tourism, Bharat Gaurav trains, holiday packages, luxury trains, and domestic travel can create more revenue opportunities.

- Rail Neer growth: Packaged drinking water is an important part of IRCTC’s physical business. Better capacity utilisation and new demand from railway passengers can help this segment.

- Technology improvement: Faster booking systems, improved mobile apps, payment integration, customer analytics, and digital travel services can improve user experience.

- Navratna status: IRCTC received Navratna status in March 2025. This can provide better operational and financial flexibility for expansion decisions.

- Strong balance sheet: The company has low debt, healthy margins, and strong return ratios. This reduces financial risk compared with many infrastructure companies.

- Cross-selling opportunity: IRCTC can sell train tickets along with hotels, flights, buses, insurance, food, lounges, and tourism packages.

- Large long-term market: India’s railway passenger system serves a huge population. Even a small increase in ticketing, travel, catering, and tourism spending can create meaningful growth.

IRCTC Share Price Target 2026–2050

The following targets are estimates based on possible revenue growth, earnings growth, passenger travel demand, business expansion, valuation levels, and wider market conditions. These are not guaranteed prices.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹500 | ₹550 | ₹600 |

| 2027 | ₹520 | ₹570 | ₹595 |

| 2028 | ₹580 | ₹645 | ₹700 |

| 2029 | ₹745 | ₹795 | ₹8,22 |

| 2030 | ₹860 | ₹942 | ₹1,080 |

| 2035 | ₹1,390 | ₹1,640 | ₹1,970 |

| 2040 | ₹3,265 | ₹3,600 | ₹3,850 |

| 2050 | ₹7,605 | ₹7,680 | ₹7,804 |

These projections assume that IRCTC maintains a healthy earnings profile, grows its travel and ticketing business, manages competition, and avoids major policy disruptions.

IRCTC Share Price Target 2026

As of July 2026, IRCTC is trading much below its 52-week high. The stock may remain volatile because investors are watching revenue growth, ticketing income, tourism demand, catering margins, and dividend announcements.

A recovery is possible if quarterly earnings remain steady and market confidence improves. However, the stock may not move sharply unless profit growth becomes stronger than current expectations.

| Period | Estimated Target Price |

|---|---|

| Second Half, July–December | ₹₹600 |

IRCTC Share Price Target 2030

By 2030, IRCTC could benefit from higher railway passenger traffic, more digital bookings, premium train services, tourism packages, Rail Neer growth, and wider use of online travel products.

The company may also benefit from deeper integration of ticketing, hotels, flights, buses, catering, payment services, and customer loyalty programmes. A stable valuation multiple and steady earnings growth can support a four-digit share price over the long term.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹₹1,390 |

| Second Half | ₹1,070 |

IRCTC Share Price Target 2035

The 2035 target depends heavily on IRCTC’s ability to grow beyond basic railway ticketing. Tourism, premium travel, hospitality, food delivery, payment services, and digital travel products may become more important.

If the company maintains strong profit margins and expands revenue at a healthy pace, IRCTC may create long-term value. However, investors should remember that a premium valuation can fall if earnings growth slows.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,700 |

| Second Half | ₹1,900 |

IRCTC Share Price Target 2040

By 2040, India’s railway system may become more modern, digital, and passenger-focused. IRCTC could benefit from higher travel demand, better stations, more premium routes, and a larger tourism market.

The company’s digital ticketing position can remain valuable if it continues to improve technology, service quality, payment experience, and customer trust. Long-term returns will depend on both business growth and valuation discipline.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹3,265 |

| Second Half | ₹3,850 |

IRCTC Share Price Target 2050

A 2050 estimate should be viewed very carefully because many things can change over 24 years. Government policies, railway reforms, technology, competition, passenger behaviour, and economic growth can all affect IRCTC.

In a positive long-term scenario, IRCTC may remain one of the important railway-linked consumer service businesses in India. Strong earnings growth, dividend income, and long-term digital expansion could support higher valuations.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹7,605 |

| Second Half | ₹7,805 |

Bull Case

- Strong growth in online railway bookings.

- Higher passenger traffic on premium trains.

- Expansion in tourism packages and religious travel.

- Better profitability from digital ticketing services.

- Growth in Rail Neer sales and catering contracts.

- Strong government support for railway modernisation.

- Increased domestic institutional ownership.

- Stable dividend payouts and healthy cash generation.

Bear Case

- Government policy changes affecting convenience fees or revenue-sharing arrangements.

- Slower growth in railway passenger traffic.

- Weak catering margins due to higher food and operating costs.

- Technology failures, cyber-security concerns, or customer service issues.

- Lower tourism demand during economic slowdown.

- Competition in travel booking, food delivery, hotels, and payment services.

- High valuation compared with slower future earnings growth.

- Heavy correction in railway and PSU stock sentiment.

Pros and Cons

Pros

- Strong brand and railway ecosystem position.

- High-margin online ticketing segment.

- Low debt and healthy return ratios.

- Government promoter support.

- Regular dividend-paying history.

Cons

- Policy-related business risk.

- Limited freedom compared with private companies.

- High dependence on railway passenger activity.

- Valuation can remain volatile.

- Catering and tourism margins can fluctuate.

Expert Opinion

IRCTC remains a quality railway-linked consumer services company with a profitable digital ticketing business, strong brand recall, low debt, and multiple travel-related revenue streams. Its long-term outlook depends on growth in online ticketing, premium railway travel, tourism, Rail Neer, and customer services.

The current valuation is lower than earlier peak levels, but investors should still monitor earnings growth rather than looking only at past share-price highs. Important factors to watch include quarterly revenue, internet ticketing income, operating margin, dividend payout, tourism growth, promoter holding, and government policy changes.

Also Check:

- ICICI Bank Share Price Target

- HFCL Share Price Target

- Exide Industries Share Price Target

- BHEL Share Price Target

- Adani Green Share Price Target

- Adani Power Share Price Target

Conclusion

IRCTC has a strong long-term business model because it operates in important railway passenger services. Its online ticketing segment, catering operations, Rail Neer business, tourism offerings, and government connection give it a unique position in the Indian market.

The company has shown steady revenue and profit growth, although the stock price has remained volatile. Long-term potential exists if passenger travel, digital services, tourism, and premium train operations continue to grow.

However, investors should also consider valuation risk, policy changes, competition, and quarterly margin pressure before making any decision.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions

1. What is the IRCTC Share Price Target for 2026?

The estimated IRCTC share price target for 2026 is ₹500 on the lower side, ₹590 on average, and ₹680 in a positive market scenario.

2. What is the IRCTC Share Price Target for 2030?

The estimated IRCTC share price target for 2030 is around ₹820 to ₹1,180, with an average estimate near ₹1,000.

3. Is IRCTC a good long-term investment?

IRCTC has strong long-term business potential because of its ticketing, railway catering, tourism, Rail Neer, and digital travel services. However, valuation and government policy risks should be considered.

4. What are the major risks of investing in IRCTC?

Major risks include government policy changes, slower railway travel growth, lower catering margins, technology issues, competition, and stock-market volatility.

5. Can IRCTC reach new all-time highs by 2030?

IRCTC can reach new highs by 2030 if profit growth improves, tourism demand increases, digital ticketing remains strong, and market valuation stays healthy. This is not guaranteed.

6. Should beginners invest in IRCTC stock?

Beginners should first understand IRCTC’s business model, valuation, risks, and share-price volatility. It is important to avoid investing only because the company is linked with Indian Railways or because of past share-price performance.