Bajaj Housing Finance is one of India’s fast-growing housing finance companies. It provides home loans, loans against property, developer finance, lease rental discounting, and other mortgage-related products. The company is part of the Bajaj group and benefits from a strong brand name, large customer base, and access to funding support.

Investors follow Bajaj Housing Finance because India’s housing loan market is expanding due to rising incomes, urbanisation, government housing support, and demand for residential properties. The company has reported steady growth in assets under management, income, and profit. This article explains Bajaj Housing Finance’s business model, financial position, shareholding pattern, historic performance, growth opportunities, risks, and estimated share price targets from 2026 to 2050.

Bajaj Housing Finance Share Overview

| Company Essential | Value |

|---|---|

| Market Cap | ₹72,908 Cr. |

| Enterprise Value | ₹1,70,000 Cr. (Approx.) |

| No. Of Shares | 832.92 Cr. |

| P/E | 28.4 |

| P/B | 3.24 |

| Face Value | ₹10 |

| Book Value | ₹27.03 |

| Debt | ₹1,46,000 Cr. (Approx.) |

| Sales Growth | 15.9% (YoY) |

| ROE | 12.1% |

| Dividend Yield | 0.00% |

What Does Bajaj Housing Finance Do?

Bajaj Housing Finance is a non-deposit-taking housing finance company. Its main business is lending money to individuals and businesses for property-related needs. The company offers home loans for buying, constructing, renovating, or extending houses. It also provides loans against property, developer financing, lease rental discounting, and financing for commercial real estate.

The company earns most of its income from interest charged on loans. It borrows funds from banks, bonds, debentures, and other sources, then lends those funds to customers at higher interest rates. The difference between borrowing cost and lending income supports profitability.

Bajaj Housing Finance has a strong advantage because of the Bajaj brand, digital loan processing, customer trust, and access to a large distribution network. Its strategy is focused on growing the loan book while maintaining strict credit quality.

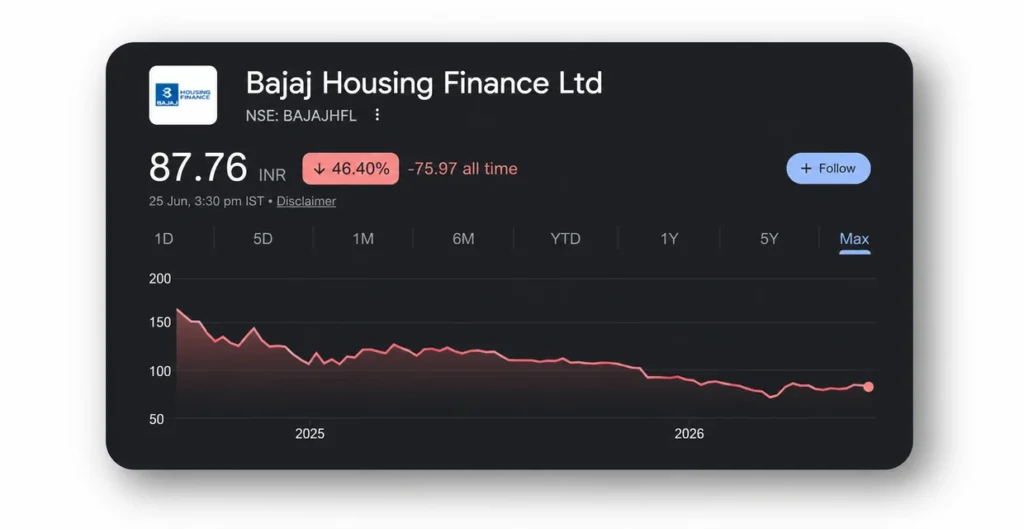

Historic Share Price Performance

Bajaj Housing Finance entered the stock market through its IPO in September 2024. The issue price was ₹70 per share, and the listing attracted strong investor interest because of the Bajaj group brand, housing finance growth potential, and the company’s strong profitability.

The stock listed at a large premium and initially saw high demand. However, after the sharp listing rally, the share price became volatile. Investors started focusing more on valuation, loan book growth, profit growth, interest rates, and asset quality.

The company’s stock performance has shown that a strong business does not always mean a straight-line share price rise. Bajaj Housing Finance has remained under close watch because it is a relatively new listed housing finance company with high promoter holding and a growing institutional investor base.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2024* | ₹150 | ₹125 | -16.7% |

| 2025 | ₹125 | ₹95 | -24.0% |

| 2026** | ₹95 | Around ₹88 | -7.4% |

* Listed in September 2024.

** Based on available 2026 market data; year is not complete.

Latest Shareholding Pattern

Bajaj Housing Finance Shareholding Pattern

| Shareholder | Holding |

|---|---|

| Promoters | 86.70% |

| FIIs | 0.99% |

| DIIs | 0.83% |

| Public | 11.14% |

| Others | 0.34% |

The promoter holding remains very high, which reflects strong control by the Bajaj group. However, investors should also track future promoter dilution because listed companies must comply with minimum public shareholding requirements over time.

Growth Factors

- Growing housing loan market: India’s housing finance sector can grow as more people buy homes in cities and semi-urban areas.

- Strong Bajaj brand: The Bajaj group has a trusted name in financial services. This can help Bajaj Housing Finance attract customers at a lower cost.

- Fast AUM growth: Assets under management reached around ₹1.41 lakh crore by the end of FY2026, showing strong loan demand.

- Home ownership demand: Rising middle-class income, nuclear families, and better access to credit can increase demand for home loans.

- Digital lending: Online loan applications, digital document verification, and faster processing can improve customer experience and reduce operating costs.

- Low bad-loan level: Gross NPA remained around 0.27% and net NPA around 0.11% at the end of FY2026. This indicates healthy loan quality.

- Improving operating efficiency: Operating expenses as a percentage of income improved in FY2026, supporting margins and profit growth.

- Cross-selling opportunity: The Bajaj ecosystem may help the company reach existing customers of Bajaj Finance and Bajaj Finserv.

- Expansion into new markets: The company can grow in Tier-2 and Tier-3 cities where home ownership demand is increasing.

- Strong capital position: Capital adequacy remained comfortable, giving the company room to grow its lending book.

Bajaj Housing Finance Share Price Target 2026 To 2050

The following estimates are based on possible growth in housing finance demand, loan book expansion, profitability, asset quality, interest-rate conditions, and valuation multiples. These are not guaranteed prices.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹73.05 | ₹69.42 | ₹98.14 |

| 2027 | ₹86.16 | ₹59.11 | ₹72.07 |

| 2028 | ₹71.40 | ₹95 | ₹65 |

| 2029 | ₹62 | ₹155 | ₹86 |

| 2030 | ₹98.60 | ₹185 | ₹139 |

| 2035 | ₹212.20 | ₹365 | ₹269.32 |

| 2040 | ₹522 | ₹650 | ₹690.10 |

| 2050 | ₹1,050.05 | ₹1,600 | ₹1,460.60 |

Also Check:

Bajaj Housing Finance Share Price Target 2026

Bajaj Housing Finance may remain volatile in 2026 because the market is still deciding the right valuation for the company. The stock’s future movement may depend on quarterly loan growth, net interest margin, borrowing cost, bad-loan control, and broader market conditions.

If profit growth remains healthy and the company continues to maintain strong asset quality, the stock may recover from lower levels. However, high valuation expectations can limit fast upside.

| Period | Estimated Target Price |

|---|---|

| First Half (Jan–Jun) | ₹73.5 – ₹85 |

| Second Half (Jul–Dec) | ₹87.67 – ₹98.14 |

Bajaj Housing Finance Share Price Target 2030

By 2030, Bajaj Housing Finance could benefit from several years of compounding in the mortgage market. India’s housing demand, improving affordability, and expansion in smaller cities may support loan book growth.

The company will need to maintain healthy margins and credit quality while growing faster than the industry. If return on equity improves and institutional ownership increases, the market may give the company a stronger valuation.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹98.60 – ₹105 |

| Second Half | ₹114.68 – ₹139.45 |

Bajaj Housing Finance Share Price Target 2035

The 2035 target depends on whether Bajaj Housing Finance can remain among the leading housing lenders in India. A larger AUM base, stable cost of funds, wider branch network, digital distribution, and disciplined underwriting may support long-term earnings growth.

At this stage, the company may have more mature operations and stronger brand reach in both metro and non-metro markets. Still, competition from banks and NBFCs may keep pressure on margins.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹212.20 – ₹241.44 |

| Second Half | ₹253.90 – ₹269.32 |

Bajaj Housing Finance Share Price Target 2040

The 2040 outlook is based on long-term economic growth, rising housing ownership, higher credit penetration, and sustained company execution. A housing finance company can create strong shareholder value when its loan book grows consistently without a major rise in defaults.

Bajaj Housing Finance will need to keep funding costs controlled, maintain a strong capital base, and avoid excessive exposure to risky real-estate segments. A steady improvement in return ratios could support the stock over this period.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹522 – ₹563.40 |

| Second Half | ₹582.11 – ₹690.10 |

Bajaj Housing Finance Share Price Target 2050

A forecast until 2050 involves significant uncertainty. Economic cycles, interest rates, regulation, real-estate demand, competition, and management decisions can change over such a long period.

Under a positive long-term case, Bajaj Housing Finance could become a much larger mortgage lender with a significantly higher loan book and profit base. However, investors should avoid treating long-term price targets as fixed outcomes. These estimates assume sustainable earnings growth and disciplined risk management over many years.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,050.05 – ₹1,1,53.77 |

| Second Half | ₹1,353.90 – ₹1,460.60 |

Bull Case

- Home loan demand grows faster than expected in India.

- Assets under management continue growing above the industry average.

- Net interest margin remains stable despite changes in interest rates.

- Bad loans remain low even during economic slowdowns.

- Return on equity improves as the company scales up.

- Bajaj group brand helps reduce customer acquisition costs.

- Digital lending improves operating efficiency.

- Higher institutional participation supports valuation expansion.

Bear Case

- Interest rates rise sharply and reduce home-loan demand.

- Borrowing costs increase faster than lending rates.

- Competition from banks puts pressure on loan yields.

- Real-estate slowdown affects property prices and loan demand.

- Bad loans rise due to weaker borrower repayment capacity.

- High promoter holding may create future share-supply concerns.

- The stock may remain expensive compared with earnings growth.

- Regulatory changes may affect capital requirements or lending rules.

Pros and Cons

Pros

- Strong Bajaj group backing.

- Fast-growing housing finance loan book.

- Healthy asset quality.

- Good profit growth in recent years.

- Digital lending and customer-service capabilities.

Cons

- The stock is relatively new in the listed market.

- High promoter holding may lead to future dilution.

- Competition from banks is intense.

- Housing finance margins can be affected by interest rates.

- No dividend payout at present.

Expert Opinion

Bajaj Housing Finance has a strong business foundation, supported by a trusted promoter group, growing assets under management, low bad loans, and good profitability. The company’s long-term outlook depends on its ability to grow loans without reducing credit standards.

The current valuation should be compared with earnings growth, book value growth, return on equity, and asset quality. Investors may track quarterly AUM growth, net interest income, cost of funds, gross NPA, net NPA, capital adequacy, and promoter shareholding changes. The stock may suit investors who understand that housing finance companies can face short-term volatility due to interest-rate and real-estate cycles.

Conclusion

Bajaj Housing Finance has emerged as an important listed player in India’s housing finance sector. Its strong Bajaj brand, growing loan book, low bad-loan ratio, improving cost efficiency, and rising profits create a positive long-term business picture.

The company may benefit from India’s rising housing demand and increased credit access in smaller cities. However, investors should also consider risks such as valuation pressure, interest-rate changes, competition, property-market slowdowns, and future promoter stake reduction.

The share price targets from 2026 to 2050 are only estimated scenarios. Actual returns can be very different depending on company performance and market conditions.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

What is the Bajaj Housing Finance Share Price Target for 2026?

The estimated Bajaj Housing Finance share price target for 2026 is around ₹85 to ₹98. Actual market performance may differ due to interest rates, quarterly results, and overall stock-market conditions.

What is the Bajaj Housing Finance Share Price Target for 2030?

The estimated target for 2030 is around ₹98 to ₹139.45. This estimate assumes continued growth in housing loans, controlled bad-loan levels, stable profitability, and a healthy Indian real estate market.

Is Bajaj Housing Finance a good long-term investment?

Bajaj Housing Finance has strong long-term business factors such as Bajaj group support, housing loan demand, low bad loans, and a growing loan book. However, long-term investors should monitor valuation, return on equity, margins, and future shareholding changes.

What are the major risks of investing in Bajaj Housing Finance?

Major risks include higher interest rates, rising borrowing costs, competition from banks, real-estate slowdown, weaker loan demand, increase in bad loans, and future promoter stake dilution.