BPCL means Bharat Petroleum Corporation Limited. It is one of India’s biggest government-owned oil companies. The company sells petrol, diesel, LPG gas cylinders, aviation fuel, lubricants, and many other fuel products.

Many investors follow BPCL shares because the company has a large fuel network, strong Bharatgas business, refineries, and government support. BPCL also gives dividends in many years, which attracts long-term investors.

However, the BPCL share price can move up and down quickly. Its profit depends on crude oil prices, fuel prices, refinery profit, government rules, and demand for petrol and diesel.

In this article, you will understand BPCL’s business, financial position, shareholding, growth chances, risks, and BPCL share price target from 2026 to 2050 in very simple English.

BPCL Share Overview & Financial Highlights

| Company Essential | Value |

|---|---|

| Market Cap | ₹1,33,865 Cr. |

| Enterprise Value | ₹1,49,600 Cr. (Approx.) |

| No. Of Shares | 432.52 Cr. |

| P/E | 5.12 |

| P/B | 1.34 |

| Face Value | ₹10 |

| Book Value | ₹231.04 |

| Debt | ₹15,735 Cr. (Approx.) |

| Sales Growth | 1.37% |

| ROE | 28.80% |

| Dividend Yield | 5.67% |

What Does BPCL Do?

Bharat Petroleum Corporation Limited (BPCL) is one of India’s leading oil and gas companies. Its main business is buying crude oil and refining it into essential petroleum products such as petrol, diesel, LPG, aviation turbine fuel, lubricants, and industrial fuels. These products are supplied to millions of customers through a large network of fuel stations, while LPG is marketed under the well-known Bharatgas brand for household cooking. Apart from retail customers, BPCL also supplies fuel to airlines, railways, defence services, factories, transport companies, and other industries across the country.

The company operates major refineries in Mumbai, Kochi, and Bina, helping it meet India’s growing energy demand. In addition to its traditional fuel business, BPCL is expanding into cleaner energy solutions by investing in electric vehicle charging infrastructure, natural gas, biofuels, renewable energy projects, and green hydrogen to support the country’s transition toward sustainable energy.

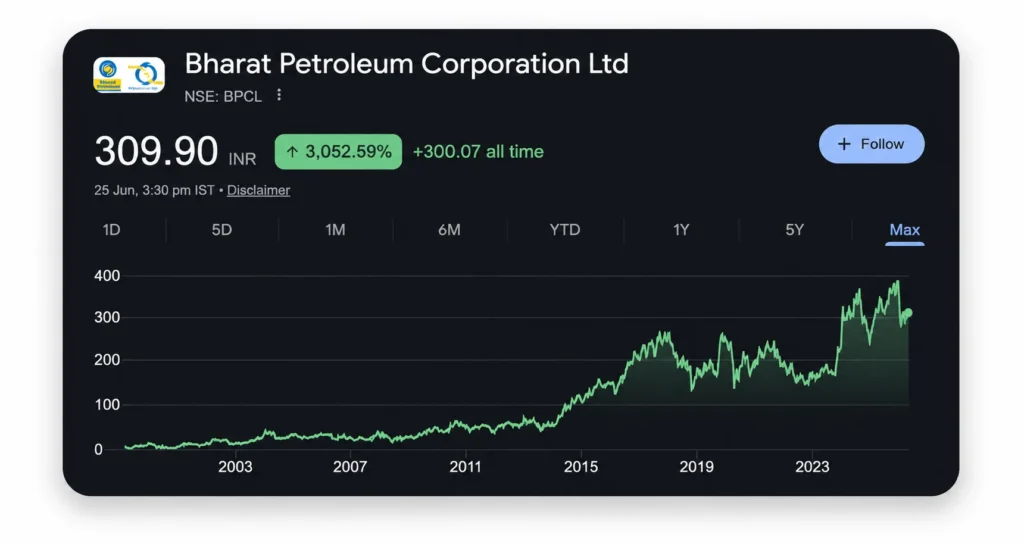

Historic Share Price Performance

- BPCL has been listed on the Indian stock market for many years and has experienced both strong rallies and sharp price corrections over time.

- The company is not a high-growth technology business. Its earnings mainly depend on crude oil prices, refining margins, and government fuel pricing policies.

- When crude oil prices remain stable and refinery margins are healthy, BPCL’s profits usually improve, which can support a rise in its share price.

- If crude oil prices increase rapidly or fuel prices cannot be adjusted accordingly, the company’s marketing margins may decline, affecting overall profitability and investor sentiment.

- BPCL has issued bonus shares in the past, which changed its historical share price. Therefore, investors should always consider bonus adjustments while analyzing old price charts.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2021 | Around ₹385 | Around ₹395 | Small gain |

| 2022 | Around ₹395 | Around ₹335 | Negative return |

| 2023 | Around ₹335 | Around ₹435 | Strong gain |

| 2024 | Around ₹435 | Around ₹295 | Negative return |

| 2025 | Around ₹295 | Around ₹305 | Mostly stable |

| 2026* | Around ₹305 | Around ₹310 | Stable to positive |

*The 2026 figure is based on the latest available market period. It can change as the year continues.

Shareholding Pattern

Promoters means the main owners of the company. In BPCL, the Government of India is the main promoter.

FIIs are foreign investors. DIIs are Indian mutual funds, insurance companies, and other Indian institutions.

High promoter holding shows that the government has strong control over BPCL. Foreign and Indian institutions also own a meaningful part of the company.

Growth Factors

- Growing fuel demand: India is still growing. More cars, trucks, buses, factories, and flights can increase demand for petrol, diesel, and aviation fuel.

- Large petrol pump network: BPCL has many fuel stations across India. More fuel sales from these stations can support income.

- Strong Bharatgas brand: Bharatgas is one of the major LPG gas brands in India. LPG demand can remain steady because it is used for cooking in homes.

- Refinery growth: BPCL is improving and expanding refinery capacity. More refinery output can help the company sell more fuel products.

- Aviation fuel demand: Air travel is growing in India. This can increase demand for aviation fuel.

- Natural gas business: BPCL is also working in natural gas and LNG. Gas demand may grow because it is cleaner than many other fuels.

- Electric vehicle charging: BPCL is setting up EV charging stations. This can help the company earn from future electric vehicle growth.

- Biofuel and green energy: BPCL is working in biofuels, renewable energy, and green hydrogen. These areas may become important in the future.

- Strong government position: BPCL is important for India’s fuel supply and energy security. This gives the company a strong place in the market.

- Dividend potential: BPCL has paid dividends in many years. Dividend income can be useful for long-term investors.

BPCL Share Price Target 2026 To 2050

The BPCL share price targets given below are only estimates. They are not fixed prices and are not guaranteed.

These targets are based on BPCL’s business size, future fuel demand, refinery performance, crude oil prices, company profit, dividend potential, and overall Indian economy growth.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹270.40 | ₹310.83 | ₹390.55 |

| 2027 | ₹397.22 | ₹362.73 | ₹356.82 |

| 2028 | ₹345.19 | ₹290 | ₹274.66 |

| 2029 | ₹285.73 | ₹355.16 | ₹398.60 |

| 2030 | ₹429.61 | ₹575.25 | ₹660.63 |

| 2035 | ₹920.40 | ₹1,040 | ₹1,164.12 |

| 2040 | ₹1,986 | ₹2,194 | ₹2,360.64 |

| 2050 | ₹4,595.40 | ₹4,893.04 | ₹5,344.20 |

Also Check:

BPCL Share Price Target 2026

BPCL share price in 2026 may depend mainly on crude oil prices, petrol and diesel demand, refinery margins, and government policy.

When crude oil prices are low or stable, BPCL may earn better marketing profit. When refinery margins remain healthy, profit can also improve.

But if crude oil becomes expensive very quickly, BPCL may face pressure. This is why investors should not expect the share to rise every month.

| Period | Estimated Target Price |

|---|---|

| First Half (Jan–Jun) | ₹270.40 to ₹312.20 |

| Second Half (Jul–Dec) | ₹315 to ₹390.55 |

BPCL Share Price Target 2030

By 2030, BPCL may benefit from higher fuel demand in India. The company may also grow through refinery expansion, LPG sales, natural gas, aviation fuel, and fuel retail outlets.

BPCL’s new business areas such as EV charging, biofuel, and renewable energy may also become more important by then.

Still, electric vehicles may reduce petrol demand in some cities. BPCL will need to grow its new energy business along with its traditional fuel business.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹429.61 to ₹496.43 |

| Second Half | ₹505 to ₹₹660.63 |

BPCL Share Price Target 2035

By 2035, BPCL may become more than only a petrol and diesel company. It may earn more from gas, renewable power, green hydrogen, EV charging, and biofuel.

The company’s strong fuel network can help it sell new energy products in the future.

However, BPCL will need to spend a large amount of money for new projects. Investors should watch whether this spending gives good returns or increases debt too much.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹920.40 to ₹1,025 |

| Second Half | ₹1,036 to ₹1,164.12 |

BPCL Share Price Target 2040

By 2040, the energy sector may change a lot. Petrol and diesel may still be used, but electric vehicles, gas, hydrogen, and renewable energy may have a bigger role.

BPCL has a good chance to remain important because it already has refineries, fuel stations, LPG customers, and a strong brand.

But its long-term success will depend on how well it changes with new technology and changing fuel demand.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,986 to ₹1,152.20 |

| Second Half | ₹1,163.05 to ₹2,360.64 |

BPCL Share Price Target 2050

A target for 2050 has a high level of uncertainty. Nobody can know exactly what crude oil prices, fuel demand, transport systems, or government rules will be after many years.

BPCL may still be a large energy company by then, but the company’s business may be very different from today.

The company may earn more from clean energy, gas, electric vehicle charging, hydrogen, and renewable power.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹4,595.40 to ₹4,864 |

| Second Half | ₹4,875 to ₹5,344.20 |

Bull Case

- India’s fuel demand grows faster than expected.

- Crude oil prices remain stable or low.

- BPCL earns strong refinery profit.

- Petrol pump sales increase every year.

- Bharatgas customers continue to grow.

- Aviation fuel demand rises because of more flights.

- EV charging and renewable energy business grow well.

- BPCL pays regular and strong dividends.

Bear Case

- Crude oil prices rise sharply.

- BPCL cannot increase fuel prices when costs rise.

- Refinery margins become weak.

- Government policy affects fuel marketing profit.

- LPG subsidy-related losses increase.

- Electric vehicles reduce petrol demand faster than expected.

- Large expansion projects increase debt.

- Global economic slowdown reduces fuel demand.

Pros and Cons

Pros

- One of India’s biggest oil companies.

- Strong government support.

- Large petrol pump network.

- Bharatgas is a trusted LPG brand.

- A dividend-paying company in many years.

Cons

- Profit depends heavily on crude oil prices.

- Government policy can affect earnings.

- Refinery business can be cyclical.

- Large expansion projects need big investment.

- Future EV growth can affect petrol demand.

Expert Opinion

BPCL is a large and important energy company, but it is not a simple stock for beginners. Its profit can change quickly because crude oil prices and refinery margins change often.

The share may look cheap when profit is high, but earnings may fall in the next year if oil conditions become weak. So, only looking at the P/E ratio is not enough.

Long-term investors should watch crude oil prices, refinery margins, petrol and diesel sales, LPG losses, company debt, dividend payments, and BPCL’s progress in gas and renewable energy.

BPCL may suit investors who understand that energy shares can be volatile.

Conclusion

BPCL is a strong Indian oil company with a large fuel network, refineries, Bharatgas business, and government support. It can benefit from India’s growing fuel demand, aviation growth, LPG use, refinery expansion, and new energy projects.

The company also has opportunities in natural gas, electric vehicle charging, biofuels, renewable energy, and green hydrogen.

However, BPCL share has risks. Rising crude oil prices, lower refinery margins, government fuel policy, and electric vehicle growth can affect the company’s future profit.

BPCL can have long-term potential, but investors should understand its business cycle before investing.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

1. What is the BPCL Share Price Target for 2026?

The BPCL share price target for 2026 is estimated between ₹270.40 and ₹390.55 The average target is around ₹335. The actual price may change based on crude oil prices, refinery margins, fuel demand, and government policy.

2. What is the BPCL Share Price Target for 2030?

BPCL share price target for 2030 is estimated between ₹429.61 and ₹660.63 This estimate assumes steady growth in fuel demand, refinery expansion, gas business growth, and stable company profit.

3. Is BPCL a good long-term investment?

BPCL has a strong business because it has refineries, petrol pumps, Bharatgas customers, and government support. But it is a cyclical stock, so its profit can change based on crude oil prices and fuel pricing rules.

4. What are the major risks of investing in BPCL?

The main risks are high crude oil prices, low refinery margins, government control over fuel prices, LPG losses, high debt from expansion projects, and fast growth in electric vehicles.

5. Can BPCL reach new all-time highs by 2030?

BPCL can reach new highs by 2030 if fuel demand rises, refinery profits stay healthy, crude oil prices remain manageable, and BPCL’s new energy projects perform well. But there is no guarantee.

6. Should beginners invest in BPCL stock?

Beginners should first understand that BPCL share can move up and down because of crude oil prices and government policy. It may be better for long-term investors who can handle market ups and downs.