BLS International Services Ltd is a global technology-enabled services company that works mainly with governments, embassies, consulates, and citizens. The company is known for visa processing, passport services, consular services, e-governance, biometrics, attestation, and citizen service solutions. Investors follow BLS because it operates in a niche business with long-term government contracts, strong margins, and expanding international demand.

The travel, visa outsourcing, and digital government services industry has good long-term potential as countries move towards secure, faster, and technology-based public services. This article explains BLS International’s business, financial strength, shareholding pattern, risks, and realistic share price targets from 2026 to 2050.

BLS Financial Overview

| Company Essential | Value |

|---|---|

| Market Cap | ₹10,061 Cr. |

| Enterprise Value | ₹9,110 Cr. (Approx.) |

| No. Of Shares | 41.24 Cr. |

| P/E | 14.6 |

| P/B | 4.08 |

| Face Value | ₹1 |

| Book Value | ₹59.8 |

| Debt | ₹72 Cr. (Approx.) |

| Sales Growth | 52% (TTM) |

| ROE | 32.7% |

| Dividend Yield | 0.82% |

What Does BLS International Services Ltd Do?

BLS International Services Ltd provides outsourced services for governments and diplomatic missions. Its main work includes visa application centres, passport services, consular support, document attestation, e-visa support, biometric enrolment, verification services, and citizen front-end services. The company earns revenue mainly from service fees, value-added services, digital government projects, and long-term contracts with government clients.

Its business is divided into visa and consular services, digital services, citizen services, biometrics, and e-governance solutions. BLS holds a strong position because this industry needs trust, compliance, data security, physical network, technology, and execution capability. Its future strategy focuses on new government contracts, expansion in more countries, digital services, acquisitions, and higher-margin service models.

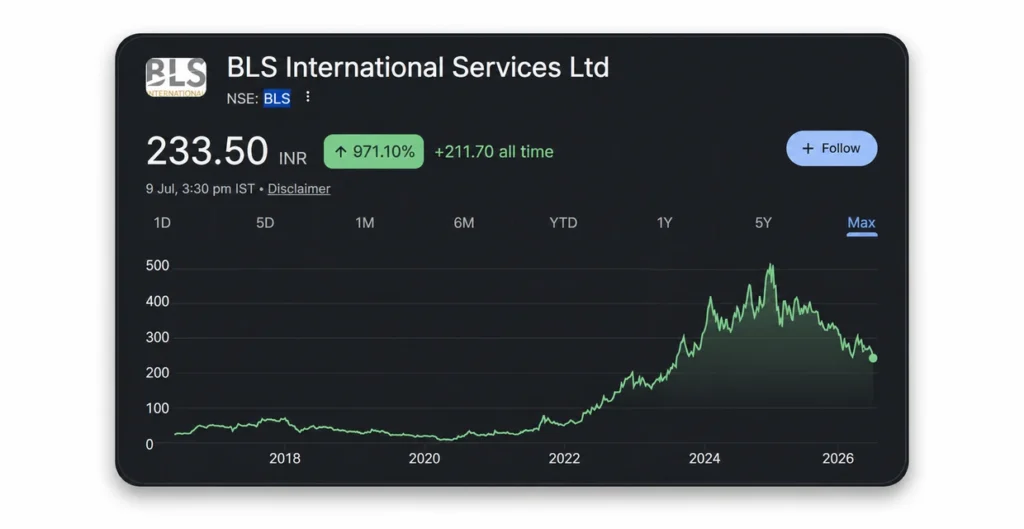

Historic Share Price Performance

BLS International has seen a strong wealth creation journey over the long term, but the stock has also remained volatile. The company benefited from growth in visa outsourcing, government services, digital platforms, and contract wins. The stock saw major rallies during 2021–2024 as earnings improved and investor interest increased in asset-light, high-margin service businesses.

However, corrections also happened when valuations became expensive, when broader small-cap and mid-cap sentiment weakened, and when regulatory or tender-related concerns affected confidence. Corporate actions such as stock splits and bonus issues also improved liquidity and made the stock more accessible to retail investors. Overall, BLS has been a strong long-term performer, but its short-term price movement can be sharp due to news flow, valuation changes, and contract-related developments.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2021 | Around ₹31 | Around ₹66 | Around 110% |

| 2022 | Around ₹67 | Around ₹165 | Around 145% |

| 2023 | Around ₹172 | Around ₹265 | Around 54% |

| 2024 | Around ₹265 | Around ₹421 | Around 59% |

| 2025 | Around ₹421 | Around ₹321 | Around -24% |

| 2026 YTD | Around ₹316 | Around ₹239 | Around -24% |

Latest Shareholding Pattern

Shareholding Pattern

The shareholding pattern shows that promoter holding remains high. This is usually seen as a sign of management confidence, but investors should also track any future reduction in promoter stake. FII holding has reduced from earlier levels, while DII participation has slowly improved. Public holding remains moderate.

Growth Factors

- Industry growth: Global visa processing, passport support, consular outsourcing, and citizen services are becoming more technology-based. This creates long-term demand for companies like BLS.

- Government initiatives: Governments are outsourcing non-core administrative work to specialized service providers for better speed, security, and efficiency.

- Global expansion: BLS operates across many countries and can grow by winning more embassy, consular, and citizen service contracts.

- Digital services: The company is expanding into e-governance, digital identity, biometric verification, and citizen service platforms.

- Better margins: The shift towards self-managed centres and digital services can support higher operating margins.

- Strong financial growth: FY2026 revenue and profit showed healthy growth, supported by visa applications, digital services, and contract execution.

- Management strategy: Expansion through new contracts, acquisitions, and technology upgrades can support long-term earnings.

- Competitive strength: BLS has experience, a wide network, government relationships, security systems, and execution capability.

- Long-term opportunities: Rising global travel, migration, digital public services, and outsourcing can support the company’s future growth.

BLS International Services Ltd Share Price Target 2026 To 2050

These share price targets are based on current fundamentals, FY2026 earnings, business growth, industry outlook, valuation comfort, and long-term compounding assumptions. These numbers assume no major stock split, bonus issue, or serious business disruption.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹240 | ₹285 | ₹330 |

| 2027 | ₹280 | ₹350 | ₹420 |

| 2028 | ₹330 | ₹430 | ₹520 |

| 2029 | ₹390 | ₹520 | ₹640 |

| 2030 | ₹470 | ₹620 | ₹780 |

| 2035 | ₹780 | ₹1,050 | ₹1,350 |

| 2040 | ₹1,150 | ₹1,600 | ₹2,100 |

| 2050 | ₹1,850 | ₹2,700 | ₹3,800 |

Also Check:

- Borosil Renewables Ltd Share Price Target

- ICICI Bank Share Price Target

- Adani Power Share Price Target

- Amara Raja Energy & Mobility Limited Share Price Target

- L&T Finance Share Price Target

- Filatex Fashions Limited Share Price Target

- Thyrocare Technologies Ltd Share Price Target

- AvenuesAI Share Price Target

- Bajaj Housing Finance Share Price Target

- IOC Share Price Target

- ITC Hotels Share Price Target

- IEX Share Price Target

BLS International Services Ltd Share Price Target 2026

For 2026, the main focus will be on earnings stability after strong FY2026 results. The stock has corrected from its higher levels, so recovery may depend on fresh contract wins, margin stability, and improved market sentiment. If the company maintains profit growth and avoids major negative news, the stock may move gradually higher. However, volatility can continue because the stock already had a strong long-term rally.

| Period | Estimated Target Price |

|---|---|

| First Half (Jan–Jun) | ₹240–₹285 |

| Second Half (Jul–Dec) | ₹285–₹330 |

BLS International Services Ltd Share Price Target 2030

By 2030, BLS International may benefit from higher visa applications, more digital government contracts, and expansion in new geographies. If revenue continues growing at a healthy pace and margins remain strong, earnings can improve meaningfully. A fair valuation multiple on higher earnings can support better stock prices. The target for 2030 remains realistic only if the company continues winning contracts and maintains strong execution.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹470–₹620 |

| Second Half | ₹620–₹780 |

BLS International Services Ltd Share Price Target 2035

The 2035 target depends on long-term business quality. If BLS becomes a larger global government services platform, its revenue base can become more diversified. More digital services, biometric solutions, and citizen service projects can improve repeat revenue. However, competitive pressure and contract renewal risk will remain important. If the company compounds earnings steadily, the stock may move into a higher long-term range.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹780–₹1,050 |

| Second Half | ₹1,050–₹1,350 |

BLS International Services Ltd Share Price Target 2040

For 2040, the estimate is based on a mature but still growing business model. BLS will need to show strong global relevance, better technology, new government contracts, and stable cash flows. If the company successfully expands beyond traditional visa services into wider citizen and digital public service solutions, the valuation can remain healthy. The downside risk will increase if growth slows or contract concentration becomes a problem.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,150–₹1,600 |

| Second Half | ₹1,600–₹2,100 |

BLS International Services Ltd Share Price Target 2050

The 2050 target is highly uncertain because it depends on business survival, leadership quality, technology changes, competition, and global public service outsourcing trends. If BLS continues to grow profitably for more than two decades, expands across digital government services, and protects margins, the stock can create long-term value. These estimates should be treated as a broad scenario, not a fixed prediction.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,850–₹2,700 |

| Second Half | ₹2,700–₹3,800 |

Bull Case

- The company wins more long-term government and embassy contracts.

- Visa and consular application volumes continue rising globally.

- Digital services become a larger part of total revenue.

- Margins remain strong due to self-managed centres and technology use.

- Acquisitions add new revenue streams and geographic reach.

- Cash flow remains healthy and debt stays under control.

- Market gives the stock a higher valuation multiple due to strong earnings growth.

- Regulatory and tender-related risks reduce over time.

Bear Case

- Any major contract loss can hurt revenue and investor confidence.

- Government tender bans, disputes, or compliance issues can create sharp corrections.

- High dependence on government contracts may create renewal risk.

- Competition may increase in visa outsourcing and digital citizen services.

- Margins may reduce if new contracts are won at lower pricing.

- Travel slowdown, geopolitical issues, or visa policy changes may affect volumes.

- Expensive acquisitions can reduce return ratios if integration fails.

- Stock valuation can remain under pressure if growth slows.

Pros and Cons

Pros

- Strong promoter holding gives stability to ownership.

- The business operates in a niche government-linked service industry.

- FY2026 revenue and profit growth were strong.

- ROE and ROCE are healthy compared with many service companies.

- Digital services and global contracts can support long-term growth.

Cons

- Stock price is volatile and has corrected sharply from highs.

- Business depends heavily on government contracts and renewals.

- Regulatory issues can affect sentiment quickly.

- Competition and pricing pressure may reduce margins.

- Long-term targets are highly uncertain because the industry can change.

Expert Opinion

BLS International Services Ltd has a strong business model, healthy return ratios, good revenue growth, and a niche position in visa, consular, and citizen services. The current valuation looks more reasonable after the correction from higher levels, but investors should not ignore the risks. The most important things to watch are contract wins, contract renewals, operating margins, cash flow, promoter holding, FII/DII activity, and any regulatory developments. The stock may suit investors who can handle volatility and understand mid-cap business risk. It should be studied with a long-term view rather than short-term price expectation.

Conclusion

BLS International Services Ltd is a strong niche player in visa outsourcing, consular support, citizen services, biometrics, and digital government solutions. The company has delivered strong financial growth and has a wide global presence. Long-term opportunities remain attractive due to rising demand for secure and technology-enabled government services. However, risks such as tender issues, contract renewals, regulatory actions, competition, and valuation changes should be carefully monitored. The share price targets from 2026 to 2050 are only estimates and may change with future results and market conditions.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

Is BLS International Services Ltd a good long-term investment?

BLS International can be considered a strong long-term stock to study because it has a niche business, global operations, strong profitability, and government-linked contracts. However, it also carries risks related to contract renewals, regulations, competition, and stock volatility.

What are the major risks of investing in BLS International Services Ltd?

The major risks include loss of key contracts, government tender restrictions, regulatory issues, lower margins, intense competition, expensive acquisitions, and a slowdown in visa or travel-related demand. Stock price volatility is also an important risk.

Can BLS International Services Ltd reach new all-time highs by 2030?

BLS International can reach new highs by 2030 if earnings continue to grow, margins remain stable, and the company wins large government contracts. However, this is not guaranteed. Market valuation, investor sentiment, and business execution will decide the actual price movement.

Should beginners invest in BLS International Services Ltd stock?

Beginners should first understand the company’s business, financials, risks, and valuation before investing. BLS is not a low-volatility stock, so fresh investors should avoid buying only because of future price targets. A disciplined approach and proper research are important.