National Aluminium Company Limited, popularly known as NALCO, is one of India’s major public-sector aluminium companies. It operates across bauxite mining, alumina refining, aluminium smelting, power generation, and downstream aluminium products.

Investors follow NALCO because aluminium demand is linked with infrastructure, electric vehicles, power transmission, railways, renewable energy, packaging, and manufacturing growth. The company also benefits from its integrated operations, including captive bauxite mines and power assets.

NALCO share price can move sharply because it depends on global aluminium prices, alumina prices, energy costs, export demand, and market sentiment. This article explains NALCO’s business, financial position, shareholding pattern, growth opportunities, risks, and estimated share price targets from 2026 to 2050.

NALCO Share Price Target Financial Highlights

| Company Essential | Value |

|---|---|

| Market Cap | ₹64,456 Cr. |

| Enterprise Value | ₹59,900 Cr. (Approx.) |

| No. Of Shares | 183.66 Cr. |

| P/E | 11.10 |

| P/B | 2.96 |

| Face Value | ₹5 |

| Book Value | ₹117.63 |

| Debt | ₹0 Cr. (Virtually Debt Free) |

| Sales Growth | 7.70% (TTM) |

| ROE | 29.40% |

| Dividend Yield | 3.02% |

The revenue and profit figures above are based on NALCO’s audited standalone FY2026 results. The market capitalization is based on the share price around ₹347.60 on 3 July 2026.

What Does National Aluminium Company Limited Do?

NALCO is an integrated aluminium company. It operates in multiple stages of the aluminium value chain, starting from bauxite mining and ending with aluminium metal and downstream products.

The company mines bauxite from its captive Panchpatmali mines in Odisha. This bauxite is used to produce alumina at its refinery. Alumina is then converted into aluminium metal at the company’s smelter plant in Angul.

NALCO also operates captive power plants and coal assets, which are important because electricity is one of the biggest costs in aluminium production. Its major revenue comes from alumina sales, aluminium metal sales, exports, wire rods, billets, and other value-added products.

Its integrated model gives NALCO a cost advantage compared with companies that depend heavily on external raw material suppliers.

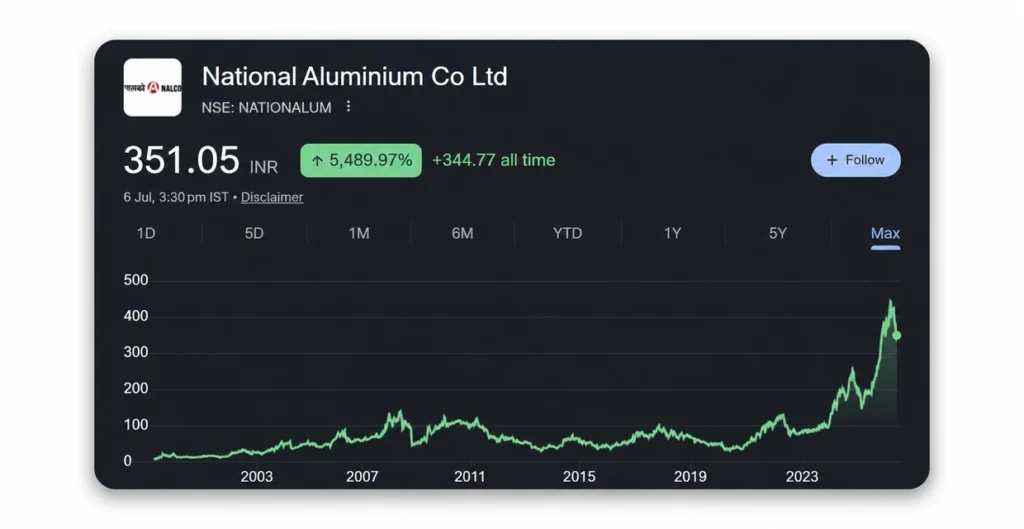

Aluminium Company Limited Share Performance

NALCO has shown a cyclical share price journey because aluminium is a commodity business. Its profits and valuation depend heavily on global aluminium prices, alumina demand, energy expenses, export conditions, and currency movement.

The stock faced pressure during 2022 when metal-sector sentiment weakened. However, NALCO saw strong recovery in 2023 and 2024 as aluminium demand improved and the company reported better operating performance.

The stock continued its positive trend in 2025, supported by higher earnings and improved business volumes. In FY2026, NALCO reported strong financial performance, but the share price also saw volatility after touching higher levels during the year. This shows that even profitable metal companies can face sharp corrections when commodity prices cool down.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2022 | ₹101.65 | ₹80.40 | -20.9% |

| 2023 | ₹81.05 | ₹131.95 | 62.8% |

| 2024 | ₹132.70 | ₹211.70 | 59.5% |

| 2025 | ₹211.15 | ₹314.30 | 48.9% |

The table uses unadjusted historical market prices and does not include dividend returns.

National Aluminium Company Limited Latest Shareholding Pattern

The Government of India remains the main promoter of NALCO. The company also has meaningful FII, mutual fund, insurance, and domestic institutional participation.

Growth Factors

- Growing aluminium demand: Aluminium demand can increase due to electric vehicles, renewable energy projects, railways, power transmission, packaging, defence, and construction activity.

- Integrated business model: NALCO has captive bauxite mines, alumina refinery operations, smelters, power plants, and coal assets. This helps reduce dependence on external raw material suppliers.

- Strong FY2026 performance: The company reported higher production, higher alumina sales, improved aluminium sales, and record annual profitability in FY2026.

- Alumina refinery expansion: NALCO has been working on its fifth alumina stream, which can increase refinery capacity after stabilization and support future alumina sales.

- Aluminium smelter expansion: The company has announced plans for a major aluminium smelter expansion. Successful execution can increase long-term aluminium production capacity.

- Downstream product opportunity: New wire rod capacity and improvements in rolled-product operations can help NALCO move towards higher-value aluminium products.

- Capex-led growth: NALCO has planned significant capital expenditure over the coming years. If projects are completed on time, future revenue and volume growth may improve.

- Government support: As a Navratna public-sector company, NALCO has strategic importance in India’s mineral and metals sector.

- Export potential: Alumina and aluminium exports can provide additional growth when international pricing and demand remain favourable.

NALCO Share Price Target 2026 To 2050

The following targets are estimated ranges, not guaranteed prices. They are based on current earnings strength, planned capacity expansion, possible aluminium demand growth, normal valuation levels, and expected commodity-market cycles.

The estimates assume that NALCO executes its refinery and smelter expansion plans without major delays, controls costs, and maintains a stable financial position. Aluminium and alumina prices will remain the biggest variables in these projections.

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹322 | ₹375 | ₹440 |

| 2027 | ₹430 | ₹405 | ₹380 |

| 2028 | ₹360 | ₹375 | ₹390 |

| 2029 | ₹395 | ₹410 | ₹438 |

| 2030 | ₹452 | ₹469 | ₹490 |

| 2035 | ₹749 | ₹810 | ₹882 |

| 2040 | ₹1,259 | ₹1,346 | ₹1,478 |

| 2050 | ₹2,654 | ₹2,774 | ₹2,972 |

NALCO’s future growth will depend on the execution of its alumina refinery expansion, smelter expansion, downstream product plans, commodity prices, and capital expenditure discipline.

NALCO Share Price Target 2026

NALCO’s 2026 outlook depends mainly on aluminium and alumina prices, domestic demand, export realizations, and quarterly earnings performance. The company entered FY2027 after reporting a strong FY2026 profit figure, but commodity prices may remain volatile.

The second half of 2026 may be important because investors will closely watch refinery expansion progress, production volumes, dividend announcements, and global aluminium pricing.

| Period | Estimated Target Price |

|---|---|

| Second Half | ₹440 |

NALCO Share Price Target 2030

By 2030, NALCO may benefit from increased alumina capacity, higher metal volumes, and growing domestic aluminium demand. However, the company may also be in the middle of a major capital expenditure cycle.

The 2030 target assumes that major expansion projects move ahead as planned and that aluminium prices remain reasonably supportive. Cost control, debt levels, and return on capital will be important factors.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹452 |

| Second Half | ₹490 |

National Aluminium Co Ltd Share Price Target 2035

The 2035 projection assumes that NALCO’s expanded refinery and smelter capacities have started contributing more meaningfully to revenue and profits. Downstream products such as wire rods and rolled products may also support better margins.

The target remains conservative because metal companies can face long commodity cycles. A weak aluminium price environment can reduce profits even if production capacity increases.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹749 |

| Second Half | ₹882 |

NALCO Share Price Target 2040

By 2040, India’s infrastructure, renewable energy, electric vehicle, power transmission, and industrial sectors may require more aluminium. NALCO could benefit if it remains cost-efficient and expands its product portfolio.

This target assumes stable operations, disciplined capital allocation, manageable debt, and continued demand for aluminium. Delays in large projects or lower international metal prices can reduce the upside.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,259 |

| Second Half | ₹1,478 |

National Aluminium Co Ltd Share Price Target 2050

A 2050 target should be viewed only as a long-term scenario, not a prediction. Over such a long period, commodity prices, government policies, technology, energy costs, global trade conditions, and competition can change significantly.

The estimate assumes that NALCO continues operating as a major integrated aluminium company, grows capacity gradually, and benefits from India’s industrial expansion. Dividend income may also add to total shareholder returns, but dividends can change every year.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹2,654 |

| Second Half | ₹2,972 |

Also Check:

- Kellton Tech Solutions Limited Share Price Target

- IRCTC Share Price Target

- ICICI Bank Share Price Target

- HFCL Share Price Target

- HCC Share Price Target

- BSE Share Price Target

- Hindustan Aeronautics Ltd Share Price Target

- GTL Infrastructure Share Price Target

- BHEL Share Price Target

Bull Case

- Aluminium and alumina prices have remained strong for several years.

- NALCO completes refinery and smelter expansion projects on time.

- Domestic aluminium demand rises faster than expected.

- Power and coal costs remain under control.

- Higher-value downstream products improve operating margins.

- Export demand supports higher alumina and aluminium sales.

- Strong profit growth leads to improved market valuation.

- Dividend payments remain attractive for long-term investors.

Bear Case

- Global aluminium prices decline sharply.

- Alumina realizations weaken due to oversupply.

- Energy, coal, freight, or raw-material costs rise significantly.

- Major expansion projects face delays or cost overruns.

- Higher capital expenditure increases debt or reduces free cash flow.

- Global recession reduces industrial metal demand.

- Government policy decisions affect capital allocation or dividends.

- Foreign institutional investors reduce exposure to commodity stocks.

Pros and Cons

Pros

- Integrated aluminium business with captive bauxite and power assets.

- Strong FY2026 revenue and profit performance.

- Government-backed Navratna public-sector company.

- Large aluminium and alumina growth opportunity.

- Potential benefit from infrastructure and renewable-energy demand.

Cons

- Earnings depend heavily on global commodity prices.

- Aluminium production requires high energy consumption.

- Large capital expenditure can affect cash flow.

- Project execution delays can reduce expected growth.

- Share price can remain volatile during weak metal cycles.

Expert Opinion

NALCO appears reasonably valued compared with its FY2026 earnings, with the stock trading near a P/E ratio of around 11 based on the latest market snapshot. However, valuation alone should not be the only factor because metal companies are cyclical.

The long-term outlook depends on aluminium and alumina prices, production growth, refinery expansion, smelter capacity addition, capital expenditure, and debt management. Investors with a higher risk appetite may track NALCO as a long-term cyclical infrastructure and metals company. Important numbers to monitor include quarterly profit, EBITDA margin, alumina realization, aluminium realization, cash flow, dividend policy, and project completion progress.

Conclusion

NALCO has strong fundamentals as an integrated aluminium producer with captive bauxite mines, refinery operations, smelters, power assets, and a government-backed business structure. Its FY2026 financial performance showed healthy revenue and profit growth.

The company has long-term growth opportunities through alumina capacity expansion, aluminium smelter projects, downstream product development, and rising demand from infrastructure and renewable energy sectors. However, investors should remember that NALCO remains a commodity-linked stock, and profits can change significantly with aluminium prices and energy costs.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

Is National Aluminium Co Ltd a good long-term investment?

NALCO has long-term potential because of its integrated aluminium business, expansion plans, and exposure to India’s infrastructure growth. However, it is a cyclical stock, so returns can be affected by aluminium prices and global demand.

What are the major risks of investing in National Aluminium Co Ltd?

The main risks include lower aluminium prices, weaker alumina demand, higher energy costs, project delays, capital expenditure pressure, government policy changes, and global economic slowdown.

Can National Aluminium Co Ltd reach new all-time highs by 2030?

NALCO can potentially reach higher levels by 2030 if aluminium demand remains strong, expansion projects are completed successfully, and earnings growth continues. However, there is no certainty because commodity prices can change quickly.