NTPC Limited is India’s largest power generation company and one of the country’s most important public sector enterprises. Established in 1975, the company has played a critical role in meeting India’s growing electricity demand through thermal, hydro, solar, wind, and other renewable energy projects. Over the years, NTPC has transformed from a conventional power producer into a diversified energy company with significant investments in green energy, hydrogen, electric mobility, and energy storage solutions.

Investors remain interested in NTPC because of its stable business model, strong government backing, predictable cash flows, and attractive dividend payouts. India’s rapidly increasing power demand, industrial growth, urbanization, and renewable energy transition provide substantial long-term opportunities for the company. NTPC’s ambitious target of expanding renewable energy capacity and becoming a major contributor to India’s clean energy goals further strengthens its future growth prospects.

With a large installed capacity, strong project pipeline, and leadership position in the Indian power sector, NTPC is widely viewed as a relatively stable long-term investment for investors seeking a combination of growth, dividends, and exposure to India’s energy infrastructure development.

Company Overview

| Particular | Details |

|---|---|

| Company Name | NTPC Limited |

| NSE Symbol | NTPC |

| BSE Code | 532555 |

| Industry | Power Generation & Utilities |

| Market Cap | ₹3.5–4.0 Lakh Crore (Approx.) |

| Founded | 1975 |

| Headquarters | New Delhi, India |

| Website | www.ntpc.co.in |

What Does NTPC Do?

NTPC Limited is India’s largest integrated power utility company. The company primarily generates electricity through coal-based thermal plants, gas-based stations, hydroelectric projects, solar farms, and wind power installations.

Its core revenue comes from selling electricity to state electricity boards, distribution companies, and industrial consumers under long-term power purchase agreements. NTPC also earns revenue from consultancy services, power trading, renewable energy projects, coal mining operations, and emerging green energy initiatives.

The company has a strong competitive advantage due to its large installed capacity, operational efficiency, government ownership, and diversified power generation portfolio. NTPC is also aggressively investing in renewable energy, green hydrogen, battery storage, and carbon reduction technologies to align with India’s clean energy transition.

NTPC Share Price Market Overview

| Metric | Value |

|---|---|

| Current Share Price | ₹360–380 (Approx.) |

| Market Capitalization | ₹3.5–4.0 Lakh Crore |

| P/E Ratio | 16–18 |

| Book Value | ₹145–160 |

| ROE | 13–15% |

| Dividend Yield | 2.5–3.5% |

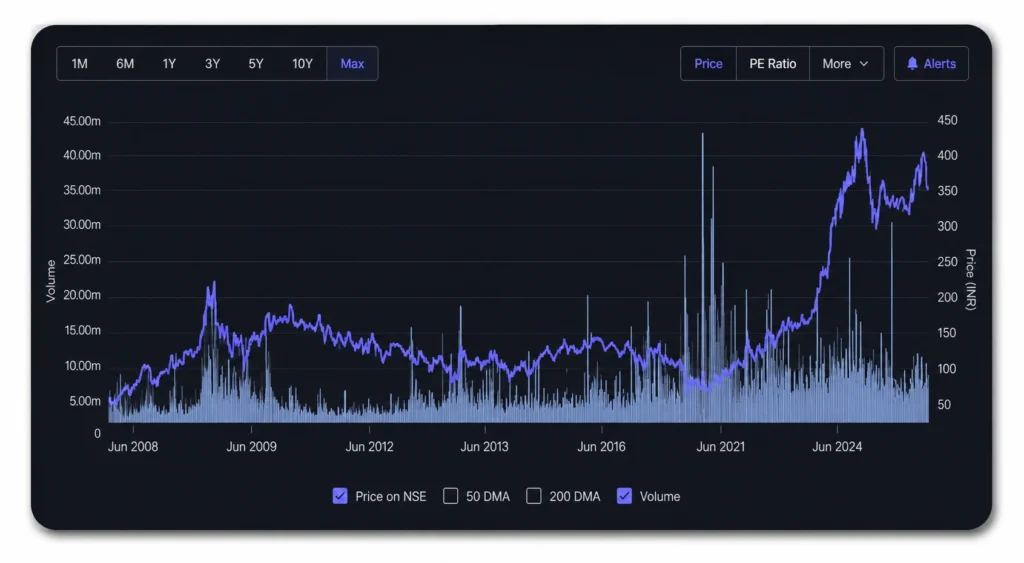

| 52-Week High | ₹448 |

| 52-Week Low | ₹292 |

| Face Value | ₹10 |

| Industry | Power & Utilities |

Financial Performance

| Financial Year | Revenue (₹ Crore) | Net Profit (₹ Crore) | EPS (₹) |

|---|---|---|---|

| FY2022 | 1,34,000 | 15,500 | 16.0 |

| FY2023 | 1,77,000 | 17,100 | 17.7 |

| FY2024 | 1,81,000 | 21,300 | 22.0 |

| FY2025 | 1,90,000+ | 22,500+ | 23.0+ |

Debt Position

NTPC operates in a capital-intensive industry and uses debt to finance large power projects.

| Metric | Value |

|---|---|

| Total Debt | ₹2.4–2.6 Lakh Crore |

| Debt-to-Equity Ratio | 1.3–1.5 |

| Interest Coverage Ratio | 3.5–4.5 |

Historic Performance

1-Year Return

Moderate positive returns supported by strong earnings and power demand growth.

3-Year Return

Significant wealth creation driven by PSU re-rating and energy demand growth.

5-Year Return

Strong multibagger performance with dividend income.

CAGR Performance

Healthy long-term CAGR supported by earnings growth and valuation expansion.

Major Price-Moving Events

- PSU stock re-rating cycle

- Rising electricity demand

- Renewable energy expansion

- Government infrastructure spending

- Record power generation

- Green hydrogen initiatives

Historical Share Price Performance

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2021 | ₹95 | ₹135 | 42% |

| 2022 | ₹135 | ₹170 | 26% |

| 2023 | ₹170 | ₹300 | 76% |

| 2024 | ₹300 | ₹335 | 12% |

| 2025 | ₹335 | ₹370+ | 10%+ |

Shareholding Pattern

| Shareholder Category | Holding |

|---|---|

| Promoters (Government of India) | ~51% |

| FIIs | ~18% |

| DIIs | ~24% |

| Public | ~6% |

| Others | Balance |

Growth Factors

- Industry Growth: India’s power demand is expected to grow steadily over the next several decades due to industrialization and urbanization.

- Expansion Plans: NTPC plans to significantly increase its installed power generation capacity.

- Capacity Additions: Large thermal, solar, hydro, and wind projects are under development.

- New Products:

- Green Hydrogen

- Battery Storage

- Renewable Energy Solutions

- Electric Mobility Infrastructure

- Government Policies: Government support for power infrastructure and renewable energy is expected to benefit NTPC.

Future Demand Drivers

- Rising electricity consumption

- EV adoption

- Data centers

- Manufacturing growth

- Renewable energy transition

Risks and Challenges

- Competition: Private power producers continue expanding their capacity.

- Regulatory Risks: Tariff regulations can impact profitability.

- Debt Concerns: High capital expenditure requires substantial borrowing.

- Economic Slowdown: Lower industrial activity could affect power demand.

- Sector Risks: Fuel costs, environmental regulations, and project delays remain key concerns.

NTPC Share Price Target 2026–2050

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹319 | ₹430 | ₹450 |

| 2030 | ₹748 | ₹760 | ₹830 |

| 2035 | ₹1,163 | ₹1,484 | ₹1,680 |

| 2040 | ₹3,580 | ₹3,894 | ₹4,205 |

| 2050 | ₹7,854 | ₹8,530 | ₹9,260 |

Also Check:

NTPC Share Price Target 2026

NTPC’s 2026 projection is based on stable power demand growth, increasing electricity consumption, and continued capacity expansion. The company is expected to benefit from rising industrial activity, infrastructure development, and higher renewable energy contributions. Strong government ownership and regulated returns provide earnings stability. Growth in green energy projects and transmission infrastructure may further support valuation expansion. Assuming consistent execution and favorable market conditions, NTPC could deliver moderate appreciation while continuing to provide dividend income to shareholders.

Monthly Target 2026

| Month | Estimated Target Price |

|---|---|

| January | ₹319 |

| February | ₹328.05 |

| March | ₹341.58 |

| April | ₹352.64 |

| May | ₹360.08 |

| June | ₹376.90 |

| July | ₹384.15 |

| August | ₹398.03 |

| September | ₹426.83 |

| October | ₹432.08 |

| November | ₹447.11 |

| December | ₹450 |

NTPC Share Price Target 2030

By 2030, NTPC is expected to have substantially increased its renewable energy capacity while maintaining leadership in power generation. Continued economic growth, electrification, and rising energy demand could support revenue growth. Green hydrogen projects and battery storage initiatives may emerge as important growth drivers. Improved operational efficiency and earnings visibility may justify higher valuations.

Monthly Target 2030

| Month | Estimated Target Price |

|---|---|

| January | ₹748 |

| February | ₹756.20 |

| March | ₹764.95 |

| April | ₹772.23 |

| May | ₹779.09 |

| June | ₹786.30 |

| July | ₹793.04 |

| August | ₹805.11 |

| September | ₹814.06 |

| October | ₹822.17 |

| November | ₹818.35 |

| December | ₹830.10 |

NTPC Share Price Target 2035

The 2035 outlook assumes NTPC successfully transforms into a diversified energy company with significant renewable and green hydrogen operations. Strong electricity demand, population growth, and industrial expansion could support earnings growth over the decade.

Monthly Target 2035

| Month | Estimated Target Price |

|---|---|

| January | ₹1,163 |

| February | ₹1,185 |

| March | ₹1,205.40 |

| April | ₹1,227.06 |

| May | ₹1,313.88 |

| June | ₹1,297.31 |

| July | ₹1,360.50 |

| August | ₹1,453.46 |

| September | ₹1,414.30 |

| October | ₹1,480.22 |

| November | ₹1,522.04 |

| December | ₹1,680 |

NTPC Share Price Target 2040

By 2040, NTPC may become one of India’s largest clean energy operators while retaining a strong conventional generation base. Technological innovation and increasing energy consumption could drive long-term growth.

Monthly Target 2040

| Month | Estimated Target Price |

|---|---|

| January | ₹3,580 |

| February | ₹3,610.02 |

| March | ₹3,654 |

| April | ₹3,731.55 |

| May | ₹3,796.30 |

| June | ₹3,825.09 |

| July | ₹3,879.41 |

| August | ₹3,964.25 |

| September | ₹4,046.89 |

| October | ₹4,126.04 |

| November | ₹4,153.03 |

| December | ₹4,205 |

NTPC Share Price Target 2050

The 2050 estimate assumes India remains one of the world’s fastest-growing energy markets. NTPC’s diversified energy portfolio, renewable leadership, and infrastructure assets could create substantial shareholder value over the long term.

Monthly Target 2050

| Month | Estimated Target Price |

|---|---|

| January | ₹7,854 |

| February | ₹7,990 |

| March | ₹8,135.06 |

| April | ₹8,253.17 |

| May | ₹8,354.90 |

| June | ₹8,530.60 |

| July | ₹8,640.05 |

| August | ₹8,775.10 |

| September | ₹8,920.04 |

| October | ₹9,002.04 |

| November | ₹9,142.73 |

| December | ₹9,260 |

Bull Case

- India’s largest power producer

- Strong government backing

- Attractive dividend yield

- Massive renewable energy pipeline

- Stable regulated business model

- Long-term energy demand growth

Bear Case

- High debt levels

- Regulatory risks

- Environmental compliance costs

- Slow renewable transition

- Fuel price volatility

Pros and Cons

Pros

- Market leader in power generation

- Consistent dividend payouts

- Strong long-term growth opportunities

Cons

- Capital-intensive business

- Regulatory dependency

- Moderate earnings growth compared to high-growth sectors

Expert Opinion

Most analysts view NTPC as a relatively stable long-term investment within the Indian utility sector. The company’s predictable cash flows, government ownership, renewable expansion plans, and dividend profile make it attractive for conservative investors. Valuation remains reasonable compared to many large-cap stocks, though growth expectations should remain moderate.

Future Outlook

NTPC’s future growth will likely be driven by India’s expanding power demand, renewable energy investments, green hydrogen initiatives, and infrastructure development. As the country moves toward cleaner energy sources, NTPC is expected to play a central role in the energy transition while maintaining its leadership position in power generation.

Conclusion

NTPC remains one of India’s most important infrastructure companies and a key player in the country’s energy sector. Its strong market position, government support, renewable energy ambitions, and stable earnings profile make it a compelling long-term investment candidate. However, investors should carefully evaluate risks related to debt, regulation, and sector dynamics before investing.

Disclaimer: This article is for educational purposes only and should not be considered financial or investment advice. Share price targets are estimates based on assumptions and may differ significantly from actual market performance.

Frequently Asked Questions (FAQs)

What is the NTPC Share Price Target for 2026?

The average estimated target for 2026 is around ₹430, with a range of ₹380–₹500.

What is the NTPC Share Price Target for 2030?

The average projected target for 2030 is approximately ₹800.

Is NTPC a good long-term investment?

NTPC is often considered a strong long-term utility stock due to its market leadership, dividend history, and growth initiatives.

What are the risks of investing in NTPC?

Major risks include regulatory changes, debt levels, fuel costs, and slower-than-expected power demand growth.

Can NTPC reach new all-time highs by 2030?

If earnings growth and renewable expansion continue as expected, NTPC could potentially achieve new highs before 2030.

Should beginners invest in NTPC stock?

Beginners seeking stable dividend-paying stocks may consider NTPC after evaluating their risk tolerance and investment objectives.