L&T Finance is one of the well-known non-banking finance companies in India. It is part of the trusted L&T group and has built a strong position in retail lending over the last few years. Many investors follow this stock because the company is growing its loan book, improving profitability, and using digital tools to scale faster. The long-term outlook for lending businesses in India remains positive because demand for home loans, rural finance, SME credit, personal loans, and two-wheeler finance is still rising. In this article, the full business model, latest financial position, shareholding pattern, past stock performance, key growth drivers, and realistic share price targets from 2026 to 2050 are explained in simple English.

L&T Finance Share Price Target Company Overview

| Company Essential | Value |

|---|---|

| Market Cap | ₹74,900 Cr. |

| Enterprise Value | ₹74,900 Cr. (Approx.) |

| No. Of Shares | 250.5 Cr. |

| P/E | 25.1 |

| P/B | 2.68 |

| Face Value | ₹10 |

| Book Value | ₹111.69 |

| Debt | ₹1,43,000 Cr. (Approx. Borrowings) |

| Sales Growth | 6.05% (5-Year CAGR) |

| ROE | 10.64% |

| Dividend Yield | 0.92% |

What Does L&T Finance Do?

L&T Finance is a retail-focused NBFC that gives loans across many categories. Its major businesses include home loans, loan against property, two-wheeler loans, personal loans, SME finance, rural business finance, farmer finance, and gold loans. The company earns money mainly from interest income, fees, and loan-related services. Over time, it has shifted away from older wholesale-heavy exposure and built a much stronger retail book. This is important because retail lending usually gives better growth visibility and wider customer reach. L&T Finance also uses digital underwriting, partnerships, data-based credit decisions, and collection systems to improve efficiency. Its competitive strength comes from the L&T brand, diversified lending book, large distribution reach, and better technology-led execution in the lending business.

Historic Share Price Performance

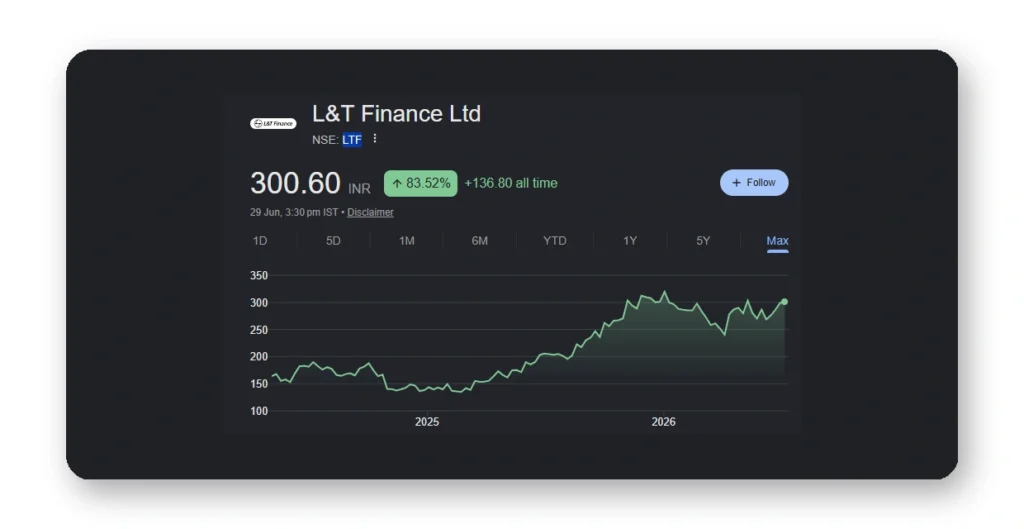

L&T Finance has had a mixed but improving stock market journey. Earlier, the stock spent many years moving slowly because the business mix was not fully retail-led and returns were not very strong. A key turning point came after the company sharpened its retail strategy and simplified the structure. The 2021 rights issue was an important capital event. Later, the merger of lending subsidiaries into one operating NBFC and the change from L&T Finance Holdings to L&T Finance improved clarity for investors. During 2023, the stock started gaining attention again. In 2024, there was consolidation and volatility. In 2025, the stock saw a strong rally as earnings, return ratios, and retail growth improved. Overall, the long-term trend has become much better than the older phase.

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2022 | ₹79.10 | ₹87.25 | 10.30% |

| 2023 | ₹89.85 | ₹165.05 | 83.70% |

| 2024 | ₹163.45 | ₹135.63 | -17.02% |

| 2025 | ₹137.76 | ₹315.95 | 129.35% |

Latest Shareholding Pattern

Growth Factors

- Strong retail lending trend: India’s retail credit market is still growing, and L&T Finance is now much more focused on retail products than before. That gives the company a wider customer base and more stable long-term growth.

- Housing and MSME demand: Demand for home loans, SME loans, and loan against property is likely to remain healthy as urbanisation and small business formalisation continue.

- Rural finance opportunity: The company has a strong presence in farmer finance and rural business finance. This gives it access to a large market that is still underpenetrated.

- Product diversification: L&T Finance is not dependent on only one loan segment. It operates across home, rural, personal, SME, gold, and vehicle-linked credit, which reduces concentration risk.

- Digital underwriting: The company is increasingly using technology, analytics, and AI-led underwriting tools. This can improve loan approval quality, speed, and operational efficiency.

- Improving financial profile: Total income, PAT, book value, and loan book have all improved in recent periods. Better return ratios support long-term valuation.

- Group brand advantage: The L&T brand gives trust, distribution support, and stronger credibility in the financial market and among borrowers.

- Cross-sell opportunity: As the customer base expands, the company can sell more than one product to the same customer, helping revenue growth without equally high acquisition costs.

- Long-term scale benefits: If the company keeps growing its high-quality retail book while controlling credit costs, profitability can rise faster than revenue over time.

L&T Finance Share Price Target 2026 To 2050

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹240 | ₹290 | ₹350 |

| 2027 | ₹325 | ₹378 | ₹430 |

| 2028 | ₹410 | ₹492 | ₹530 |

| 2029 | ₹380 | ₹423 | ₹455 |

| 2030 | ₹460 | ₹526 | ₹573 |

| 2035 | ₹748 | ₹840 | ₹858 |

| 2040 | ₹790 | ₹840 | ₹980 |

| 2050 | ₹1,873 | ₹1,990 | ₹2,348 |

Also Check:

- Thyrocare Technologies Ltd Share Price Target

- Bajaj Housing Finance Share Price Target

- IEX Share Price Target

- IFCI Share Price Target

- South Indian Bank Share Price Target

- Canara Bank Share Price Target

L&T Finance Share Price Target 2026

The 2026 outlook depends on continued book growth, stable credit cost, and healthy margins. The company already has strong momentum in retail disbursement and book expansion. If execution remains strong, the stock can stay firm. However, because the share already moved up sharply in the recent past, valuation may limit very fast upside in the near term. So, 2026 estimates should stay moderate and realistic.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹290 |

| Second Half | ₹350 |

L&T Finance Share Price Target 2030

By 2030, L&T Finance could become a much larger retail NBFC if it keeps growing in home loans, SME finance, gold loans, personal loans, and rural lending. Better technology and cross-sell can improve scale and operating efficiency. If return ratios hold near or above current levels and credit costs remain under control, valuation can remain supportive over the medium term.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹460 |

| Second Half | ₹573 |

L&T Finance Share Price Target 2035

The 2035 estimate assumes the company continues compounding its loan book and net worth for several years without major balance sheet stress. By then, the business could be more mature, more diversified, and better placed across secured and unsecured lending categories. A lot will depend on funding cost discipline, asset quality, and management execution during economic slowdowns.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹748 |

| Second Half | ₹858 |

L&T Finance Share Price Target 2040

The 2040 target is based on the assumption that L&T Finance remains a major listed retail lender with stronger scale, wider customer reach, and better earnings quality than today. Over such a long period, market cycles will come and go. So this target should be seen as a broad range, not a fixed outcome. Long-term compounding in book value will be the biggest driver.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹790 |

| Second Half | ₹980 |

L&T Finance Share Price Target 2050

The 2050 estimate is only a long-term projection based on business durability, industry growth, and the company’s ability to maintain healthy profitability. Over 20-plus years, management quality, regulation, competition, funding access, and credit discipline will matter more than short-term market sentiment. If the company compounds consistently, the stock can create meaningful long-term value, but there will also be long periods of volatility.

| Period | Estimated Target Price |

|---|---|

| First Half | ₹1,873 |

| Second Half | ₹2,348 |

Bull Case

- Retail loan book continues growing at a healthy pace for many years.

- Return on assets and return on equity improve further from current levels.

- Digital underwriting and AI tools reduce credit losses over time.

- Gold loans, SME finance, and personal loans scale faster than expected.

- Cross-sell into the existing customer base improves profitability.

- The market rewards the company with a stronger valuation multiple.

- Funding access stays comfortable due to the strong parent-group reputation.

- Asset quality remains stable even while the company grows faster.

Bear Case

- Credit cost rises sharply in rural or unsecured portfolios.

- Borrowing costs remain high and pressure margins.

- Strong competition from banks and fintech lenders reduces spreads.

- Faster growth in risky segments hurts future profitability.

- Valuation becomes expensive compared with earnings growth.

- Any regulatory tightening in digital or retail lending can slow growth.

- Economic slowdown can affect collections and new disbursements.

- Execution misses in new segments may reduce investor confidence.

Pros and Cons

Pros

- Strong promoter backing and trusted L&T group brand

- Retail-focused strategy is clearer than before

- Improving PAT, book value, and loan book

- Diversified presence across many lending segments

- Better technology-led underwriting and collections

Cons

- NBFC business remains sensitive to funding cost cycles

- Credit quality risks can rise in unsecured and rural books

- ROE is improving, but still not extremely high

- Valuation is no longer as cheap as earlier years

- Lending business is tightly linked to economic conditions

Expert Opinion

L&T Finance looks stronger today than it did a few years ago because the business mix is cleaner, retail-focused, and more profitable. Still, the stock is no longer a deep-value story, so future returns may depend more on earnings growth than on simple re-rating. Long-term investors should watch total income growth, PAT growth, book value growth, NIM plus fee income, credit cost, RoA, and RoE. Asset quality across personal, rural, SME, and gold segments will be very important. This stock may suit investors who understand NBFC cycles and are comfortable with periodic volatility, not those looking for guaranteed short-term returns.

Conclusion

L&T Finance has become a more focused and better-quality NBFC after its retail shift and business simplification. The company has strong brand support, rising scale, improving profits, and a diversified lending model. These are important strengths for long-term growth. At the same time, investors should remember that all lending businesses face risks from funding costs, regulation, economic slowdown, and asset quality pressure. If management continues executing well, the long-term outlook remains positive. But projections should always be treated as estimates, not certainty.

Disclaimer: The share price targets mentioned in this article are estimates based on current market conditions, company fundamentals, and industry trends. They should not be considered investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

Can L&T Finance reach new all-time highs by 2030?

Yes, it is possible if the company continues to improve PAT, RoA, RoE, and retail book growth. But that will depend on execution, market sentiment, and broader economic conditions.

Is L&T Finance a good long-term investment?

L&T Finance can be considered for long-term tracking because it has a strong brand, growing retail book, improving profits, and better business clarity than before. But it still carries NBFC-related risks.

What are the major risks of investing in L&T Finance?

Major risks include rising credit cost, higher borrowing costs, competition from banks and fintech companies, valuation pressure, and slower growth during weak economic periods.

Should beginners invest in L&T Finance stock?

Beginners should first understand how NBFCs work, especially margin, asset quality, and funding risk. It may be better suited to investors who can track financial results regularly and stay patient through volatility.