IDFC First Bank has emerged as one of India’s fastest-transforming private sector banks. Formed through the merger of IDFC Bank and Capital First, the bank has steadily shifted its focus toward retail banking, digital banking, consumer finance, and customer-centric banking solutions. Over the past few years, the bank has improved its deposit franchise, strengthened asset quality, expanded its branch network, and increased its retail loan portfolio.

Investors are closely watching IDFC First Bank because of its long-term growth potential, improving profitability, and strong management execution. The bank has successfully reduced its dependence on wholesale lending while building a diversified retail-focused business model. Rising CASA deposits, expanding customer base, digital banking initiatives, and improving operating efficiency are key factors supporting future growth.

As India’s banking sector continues to benefit from rising credit demand, financial inclusion, and digital adoption, IDFC First Bank is well-positioned to capture a larger market share. While challenges such as competition and economic cycles remain, the bank’s transformation journey has made it an increasingly attractive stock for long-term investors looking for growth opportunities in the Indian banking sector.

IDFC First Bank Share Price Overview

| Particular | Details |

|---|---|

| Company Name | IDFC First Bank Limited |

| NSE Symbol | IDFCFIRSTB |

| BSE Code | 539437 |

| Industry | Private Sector Banking |

| Market Cap | ₹63,000–66,000 Crore |

| Founded | 2018 (Post Merger) |

| Headquarters | Mumbai, Maharashtra |

| Website | www.idfcfirstbank.com |

What Does IDFC First Bank Do?

IDFC First Bank is a full-service private sector bank offering retail banking, corporate banking, treasury services, wealth management, loans, deposits, credit cards, and digital banking solutions.

The bank generates revenue primarily through:

- Interest income from loans

- Retail lending operations

- Credit card business

- Corporate banking services

- Treasury operations

- Fee-based income

- Wealth management services

Its core lending segments include:

- Home Loans

- Personal Loans

- Business Loans

- Vehicle Loans

- MSME Loans

- Consumer Durable Financing

- Credit Cards

The bank’s strategy focuses heavily on retail banking because retail assets generally provide better margins and lower concentration risks than wholesale lending. This transformation has strengthened the bank’s long-term growth profile.

IDFC First Bank Share Price Market Overview

| Metric | Value |

|---|---|

| Current Share Price | ₹73–78 |

| Market Capitalization | ₹63,000–66,000 Crore |

| P/E Ratio | 38–40 |

| Book Value | ₹54.7 |

| ROE | 7–9% |

| Dividend Yield | 0.35% |

| 52-Week High | ₹87 |

| 52-Week Low | ₹58 |

| Face Value | ₹10 |

| Industry | Private Sector Banking |

IDFC First Bank Share Price Target 2026 To 2050

| Year | Minimum Target | Average Target | Maximum Target |

|---|---|---|---|

| 2026 | ₹68.45 | ₹81.72 | ₹96.20 |

| 2027 | ₹93.85 | ₹112.45 | ₹128.58 |

| 2028 | ₹108 | ₹131.62 | ₹154.67 |

| 2029 | ₹124.52 | ₹159.80 | ₹190.31 |

| 2030 | ₹154.91 | ₹189.65 | ₹227.68 |

| 2035 | ₹300.42 | ₹448.36 | ₹596.70 |

| 2040 | ₹549.85 | ₹793.80 | ₹901.56 |

| 2050 | ₹1,187.44 | ₹1,692.53 | ₹2,160.30 |

Also Check:

- Tata Motors Passenger Vehicles Share Price Target

- Suzlon Energy Share Price Target

- Ashok Leyland Share Price Target

IDFC First Bank Share Price Target 2026

The 2026 target assumes that IDFC First Bank continues its retail banking expansion strategy while improving profitability and operational efficiency. Growth in retail loans, higher CASA deposits, stronger fee income, and controlled asset quality are expected to support earnings growth. India’s growing credit demand, digital banking adoption, and financial inclusion initiatives could further boost the bank’s performance.

If management successfully improves return ratios and maintains healthy loan growth, investor confidence may increase, resulting in valuation expansion. However, factors such as interest rate movements, economic conditions, and regulatory changes could influence actual performance. Based on current business fundamentals and growth expectations, the stock could trade in the range of ₹68.45 to ₹96.20 during 2026.

Monthly Target Table 2026

| Month | Estimated Target Price |

|---|---|

| January | ₹68.45 |

| February | ₹67.93 |

| March | ₹69.84 |

| April | ₹71.56 |

| May | ₹74.89 |

| June | ₹76.50 |

| July | ₹79.68 |

| August | ₹83.76 |

| September | ₹87.54 |

| October | ₹89.32 |

| November | ₹93.89 |

| December | ₹96.20 |

IDFC First Bank Share Price Target 2030

The 2030 target assumes sustained growth in retail banking, improved profitability, higher market share, and a stronger balance sheet. By 2030, the bank could benefit from increased digital banking adoption, rising consumer credit demand, and continued expansion in wealth management and credit card businesses.

The projection also assumes stable asset quality, healthy capital adequacy, and improving return on equity. If the bank successfully competes with larger private sector peers while maintaining growth momentum, its valuation could improve significantly. Under favorable conditions, the stock may trade between ₹154.91and ₹227.68 by 2030.

Monthly Target Table 2030

| Month | Estimated Target Price |

|---|---|

| January | ₹154.91 |

| February | ₹159.74 |

| March | ₹164.11 |

| April | ₹170.83 |

| May | ₹175.42 |

| June | ₹183.54 |

| July | ₹191.23 |

| August | ₹200.41 |

| September | ₹209.56 |

| October | ₹217.64 |

| November | ₹224.87 |

| December | ₹227.68 |

IDFC First Bank Share Price Target 2035

The 2035 outlook is based on the assumption that IDFC First Bank successfully evolves into one of India’s leading retail-focused private sector banks. Continuous customer acquisition, technological innovation, and expansion into higher-margin lending segments may drive earnings growth over the long term.

By this period, the bank could benefit from a larger deposit base, stronger profitability metrics, and increased cross-selling opportunities. If India’s economy maintains a healthy growth trajectory and the banking sector continues to expand, the stock may achieve substantial appreciation. The estimated range for 2035 is ₹300.42 to ₹596.70.

Monthly Target Table 2035

| Month | Estimated Target Price |

|---|---|

| January | ₹300.42 |

| February | ₹319.89 |

| March | ₹337.96 |

| April | ₹358.73 |

| May | ₹383.54 |

| June | ₹401.32 |

| July | ₹430.55 |

| August | ₹459.90 |

| September | ₹498.76 |

| October | ₹536.82 |

| November | ₹568.21 |

| December | ₹596.70 |

IDFC First Bank Share Price Target 2040

The 2040 target reflects a highly optimistic long-term scenario where the bank continues to gain market share, strengthen profitability, and successfully adapt to evolving financial technologies. Increased digital penetration, artificial intelligence-based banking services, and rising financial inclusion may create significant growth opportunities.

A larger customer base, higher return on equity, and a diversified lending portfolio could support sustained earnings growth. If the bank remains competitive and executes its strategy effectively, the stock could trade between ₹549.85 and ₹901.56 by 2040.

Monthly Target Table 2040

| Month | Estimated Target Price |

|---|---|

| January | ₹549.85 |

| February | ₹578.63 |

| March | ₹597.90 |

| April | ₹629.34 |

| May | ₹663.78 |

| June | ₹697.81 |

| July | ₹723.65 |

| August | ₹768.89 |

| September | ₹802.83 |

| October | ₹839.05 |

| November | ₹875.23 |

| December | ₹901.56 |

IDFC First Bank Share Price Target 2050

The 2050 projection represents a long-term growth scenario based on decades of economic expansion, rising banking penetration, and successful business execution. By 2050, India’s financial sector could be significantly larger than today, creating opportunities for leading private sector banks.

If IDFC First Bank maintains strong management execution, expands its product portfolio, and consistently improves shareholder returns, substantial wealth creation may be possible. While such long-term forecasts involve considerable uncertainty, the stock could potentially trade between ₹1,187.44 and ₹2,160.30 under favorable conditions.

Monthly Target Table 2050

| Month | Estimated Target Price |

|---|---|

| January | ₹1,187.44 |

| February | ₹1,248.15 |

| March | ₹1,329.20 |

| April | ₹1,402.52 |

| May | ₹1,488.67 |

| June | ₹1,569.35 |

| July | ₹1,657.19 |

| August | ₹1,754.80 |

| September | ₹1,849.16 |

| October | ₹1,958.28 |

| November | ₹2,053.90 |

| December | ₹2,160.30 |

Financial Performance

IDFC First Bank has demonstrated consistent growth in revenue, deposits, and loan book expansion. Although profitability has experienced fluctuations during the bank’s transformation phase, long-term trends remain positive.

Revenue & Profit Performance

| Financial Year | Revenue (₹ Crore) | Net Profit (₹ Crore) | EPS (₹) |

|---|---|---|---|

| FY2022 | 18,755 | 145 | 0.23 |

| FY2023 | 27,194 | 2,437 | 3.40 |

| FY2024 | 32,776 | 2,957 | 4.12 |

| FY2025 | 37,000+ | 1,600+ | 1.88 |

Debt Position

Since banks operate using deposits and borrowings, debt metrics differ from those of non-financial companies.

| Metric | Value |

|---|---|

| Total Debt/Borrowings | ₹2.7 Lakh Crore+ |

| Debt-to-Equity Ratio | Banking Industry Specific |

| Interest Coverage Ratio | Not Applicable for Banks |

Debt Analysis

The bank’s borrowings and deposits support lending operations. Investors should focus more on capital adequacy, CASA ratio, GNPA, NNPA, and loan growth rather than traditional debt ratios.

Historic Performance

Return Analysis

1-Year Return

The stock has delivered moderate returns over the past year as investors assessed profitability and asset quality trends.

3-Year Return

The bank has generated strong returns due to improving earnings, retail expansion, and balance sheet strengthening.

5-Year Return

Long-term shareholders have benefited from the successful turnaround and business transformation strategy.

CAGR Performance

The stock has produced double-digit CAGR returns over longer periods, supported by improving fundamentals.

Major Price-Moving Events

- Capital First merger integration

- Improvement in asset quality

- Growth in CASA deposits

- Expansion of retail lending

- Quarterly earnings surprises

- RBI policy changes

- Credit growth trends

- Digital banking expansion

Historical Share Price Performance

| Year | Opening Price | Closing Price | Return |

|---|---|---|---|

| 2021 | ₹35 | ₹45 | 29% |

| 2022 | ₹45 | ₹57 | 27% |

| 2023 | ₹57 | ₹85 | 49% |

| 2024 | ₹85 | ₹66 | -22% |

| 2025 | ₹66 | ₹74 | 12% |

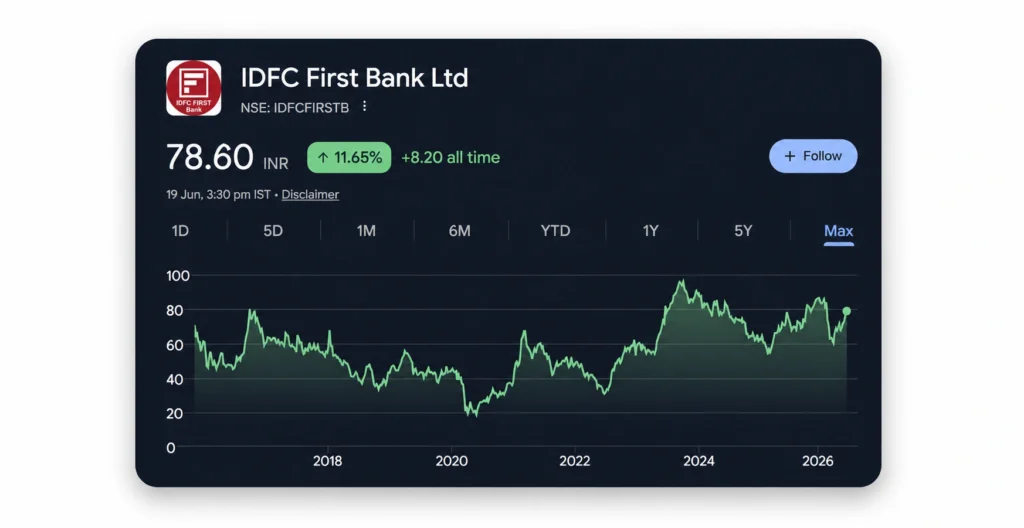

All-Time High and All-Time Low

| Metric | Value |

|---|---|

| All-Time High (ATH) | ₹100.74 |

| ATH Date | 5 September 2023 |

| All-Time Low (ATL) | ₹17.75 |

| ATL Date | 24 March 2020 |

Shareholding Pattern

Latest Available Quarter

| Shareholder Category | Holding |

|---|---|

| Promoters | 0% |

| FIIs | 26% |

| DIIs | 16% |

| Public | 53% |

| Others | 5% |

Shareholding Analysis

Unlike many private banks, IDFC First Bank does not have a traditional promoter holding structure. Institutional ownership remains strong, reflecting confidence in the bank’s transformation and future growth potential.

Growth Factors

- Industry Growth: India’s banking sector is expected to benefit from rising credit demand, urbanization, and financial inclusion.

- Expansion Plans: The bank continues to expand its branch network and digital banking capabilities.

- Capacity Additions: Growth in retail lending, credit cards, and customer acquisition remains a major focus area.

- New Products:

- Digital savings accounts

- Wealth management services

- Credit cards

- Consumer finance solutions

- MSME lending products

- Government Policies: Supportive banking regulations and financial inclusion initiatives can support long-term growth.

- Future Demand Drivers:

- Rising middle-class income

- Digital banking adoption

- Consumer credit growth

- Housing finance demand

- SME financing requirements

Risks and Challenges

Competition

The bank faces intense competition from:

- HDFC Bank

- ICICI Bank

- Axis Bank

- Kotak Mahindra Bank

- AU Small Finance Bank

Regulatory Risks

Changes in RBI regulations may impact profitability and lending growth.

Asset Quality Risks

A rise in NPAs could affect earnings and investor sentiment.

Economic Slowdown

Lower credit demand during economic downturns can reduce profitability.

Sector Risks

- Interest rate volatility

- Liquidity concerns

- Credit cycle risks

- Economic uncertainty

Bull Case

The following factors could help the stock outperform expectations:

- Strong growth in retail loans.

- Rising CASA ratio and lower funding costs.

- Improvement in ROE and profitability.

- Rapid digital banking adoption.

- Expansion of credit card business.

- Strong economic growth in India.

- Better-than-expected asset quality.

- Valuation re-rating by investors.

Bear Case

The following risks could cause the stock to underperform:

- Higher NPAs and credit losses.

- Slower loan growth.

- Margin pressure due to competition.

- Economic slowdown affecting borrowers.

- Regulatory changes impacting profitability.

- Rising interest rates reducing credit demand.

- Lower-than-expected earnings growth.

Pros and Cons

Pros

- Strong retail banking growth strategy.

- Improving deposit franchise and CASA ratio.

- Significant long-term growth potential.

Cons

- ROE remains below leading private banks.

- Intense competition from larger banks.

- Earnings can be impacted by credit cycle risks.

Expert Opinion

Many analysts view IDFC First Bank as a long-term turnaround and growth story within the Indian banking sector. The bank has made substantial progress in transforming its business model from wholesale-focused lending to a diversified retail banking franchise. Improvements in asset quality, customer acquisition, and deposit growth have strengthened investor confidence.

From a valuation perspective, the stock often trades at a discount to larger private sector peers due to its lower profitability metrics. However, if management successfully improves ROE and maintains strong growth, valuation multiples may expand over time. Long-term investors willing to tolerate short-term volatility may find the stock attractive from a growth perspective.

Future Outlook

The future outlook for IDFC First Bank remains positive due to several structural growth drivers. Rising banking penetration, digital transformation, increasing consumer credit demand, and growth in financial services are expected to support long-term expansion.

The bank’s focus on retail banking, technology-driven solutions, and customer-centric products could help it gain market share in the coming years. Continued branch expansion, stronger fee income, and improved operational efficiency may further enhance profitability.

If management continues to execute effectively, IDFC First Bank could emerge as a stronger competitor among India’s private sector banks over the next decade.

Conclusion

IDFC First Bank has undergone a significant transformation and established itself as a growing retail-focused private sector bank. The company benefits from improving asset quality, expanding retail operations, rising deposits, and increasing digital adoption. These factors provide a solid foundation for long-term growth.

While risks such as competition, economic cycles, and regulatory changes remain, the bank’s strategic direction and business improvements make it an interesting stock for long-term investors. Investors should evaluate their risk tolerance, investment horizon, and portfolio diversification before making any investment decision.

Risk Disclaimer: Share price targets are estimates based on assumptions regarding business growth, profitability, economic conditions, and market sentiment. Actual stock prices may differ significantly from these projections.

Frequently Asked Questions (FAQs)

What is the IDFC First Bank Share Price Target for 2026?

The estimated share price target for 2026 ranges between ₹80 and ₹115, with an average target of ₹95.

What is the IDFC First Bank Share Price Target for 2030?

The estimated share price target for 2030 ranges between ₹150 and ₹260, with an average target of ₹200.

Is IDFC First Bank a good long-term investment?

The bank offers long-term growth potential due to its retail banking strategy, improving profitability, and expanding customer base. However, investors should assess risks before investing.

What are the risks of investing in IDFC First Bank?

Key risks include asset quality deterioration, economic slowdowns, regulatory changes, rising competition, and pressure on profit margins.

Can IDFC First Bank reach new all-time highs by 2030?

If the bank continues improving profitability and expanding its retail banking franchise, it may potentially surpass its previous all-time high by 2030.

Should beginners invest in IDFC First Bank stock?

Beginners should consider their financial goals, risk tolerance, and investment horizon before investing. Diversification and proper research are essential when investing in banking stocks.